Articles

Posted on June 6, 2025

Weak Canadian Labour Report in May Points Towards BoC Easing

Labour Market Weakness Continued in May, Raising the Prospects of a Rate Cut at The Next BoC Meeting

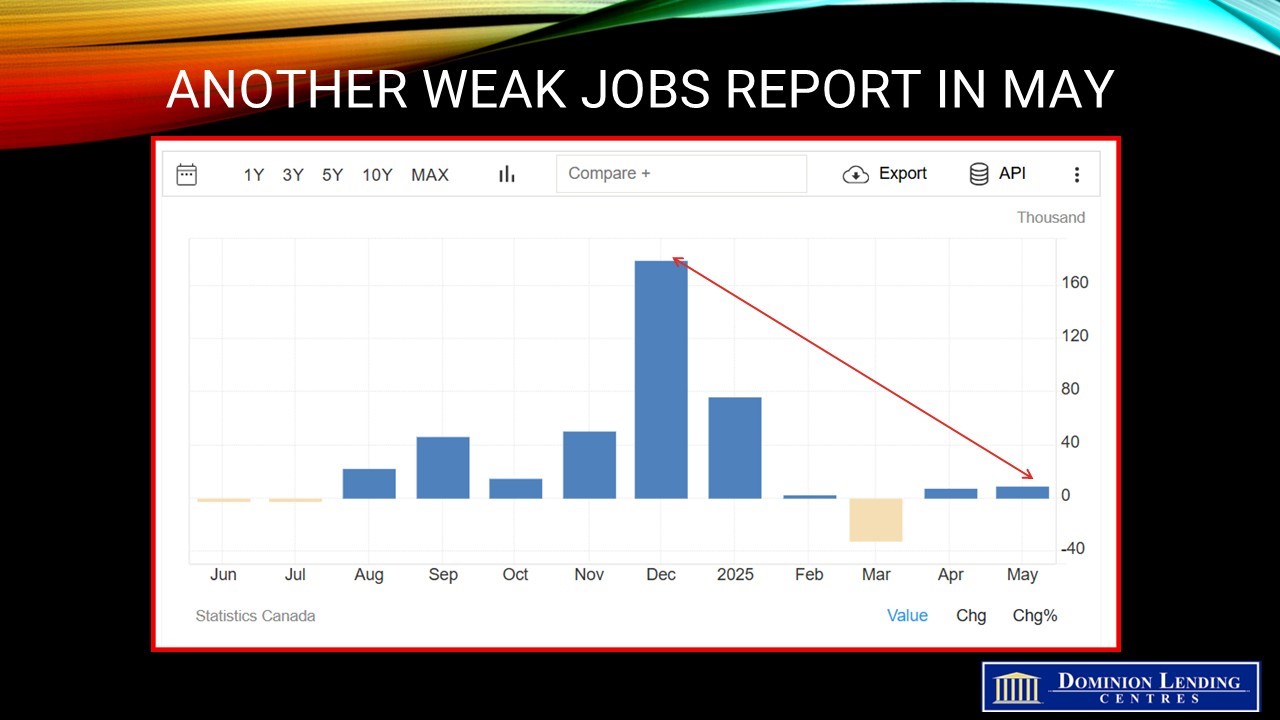

Today’s Labour Force Survey for May showed a marked adverse impact of tariffs on the Canadian economy. Employment held steady for the second consecutive month at a modest net job change of 8,800–below expectations.

Growth in full-time employment (+58,000; +0.3%) was offset by a decline in part-time work (-49,000; -1.3%). There has been virtually no employment growth since January, following substantial gains from October 2024 to January 2025 (+211,000; +1.0%).

The employment rate—the proportion of the population aged 15 and older—was unchanged at 60.8% in May, matching a recent low observed in October 2024. The employment rate had fallen for two consecutive months in March (-0.2 percentage points) and April 2025 (-0.1 percentage points).

The number of private sector employees rose by 61,000 (+0.4%) in May, the first increase since January. Public sector employment fell by 21,000 (-0.5%) in the month, following an increase in April that was partly attributable to the hiring of temporary workers for the federal election. Self-employment also fell (-30,000; -1.1%) in May, the first significant decrease since May 2023.

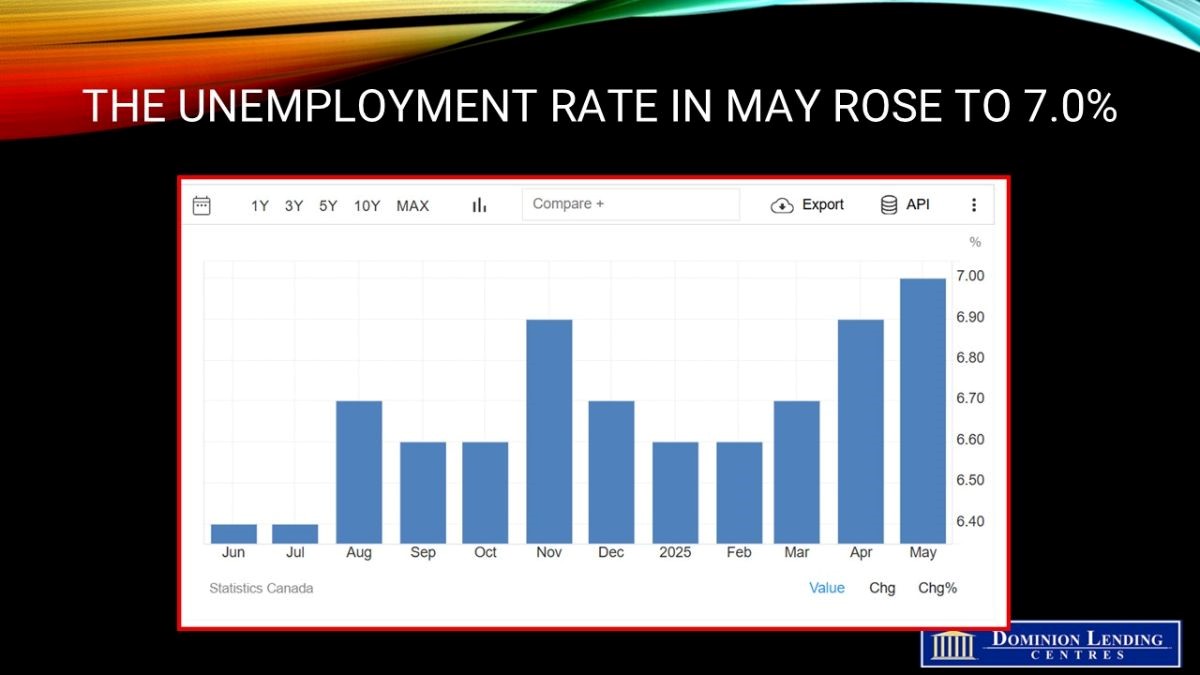

The unemployment rate increased 0.1 percentage points to 7.0% in May, the highest rate since September 2016 (excluding 2020 and 2021, during the pandemic). The uptick in May was the third consecutive monthly increase; since February, the unemployment rate has risen by 0.4 percentage points.

There were 1.6 million unemployed people in May, an increase of 13.8% (+191,000) from 12 months earlier. A smaller share of people who were unemployed in April transitioned into employment in May (22.6%), compared with one year earlier (24.0%) and compared with the pre-pandemic average for the same months in 2017, 2018 and 2019 (31.5%) (not seasonally adjusted). This indicates that people face greater difficulties finding work in the current labour market.

The average duration of unemployment has also been rising; unemployed people had spent an average of 21.8 weeks searching for work in May, up from 18.4 weeks in May 2024. Furthermore, nearly half (46.5%) of people unemployed in May 2025 had not worked in the previous 12 months or had never worked, up from 40.7% in May 2024 (not seasonally adjusted).

The layoff rate—representing the proportion of people who were employed in April but became unemployed in May as a result of a layoff—was 0.6%, unchanged from May 2024 (not seasonally adjusted).

Total hours worked were unchanged in May but were up 0.9% compared with 12 months earlier.

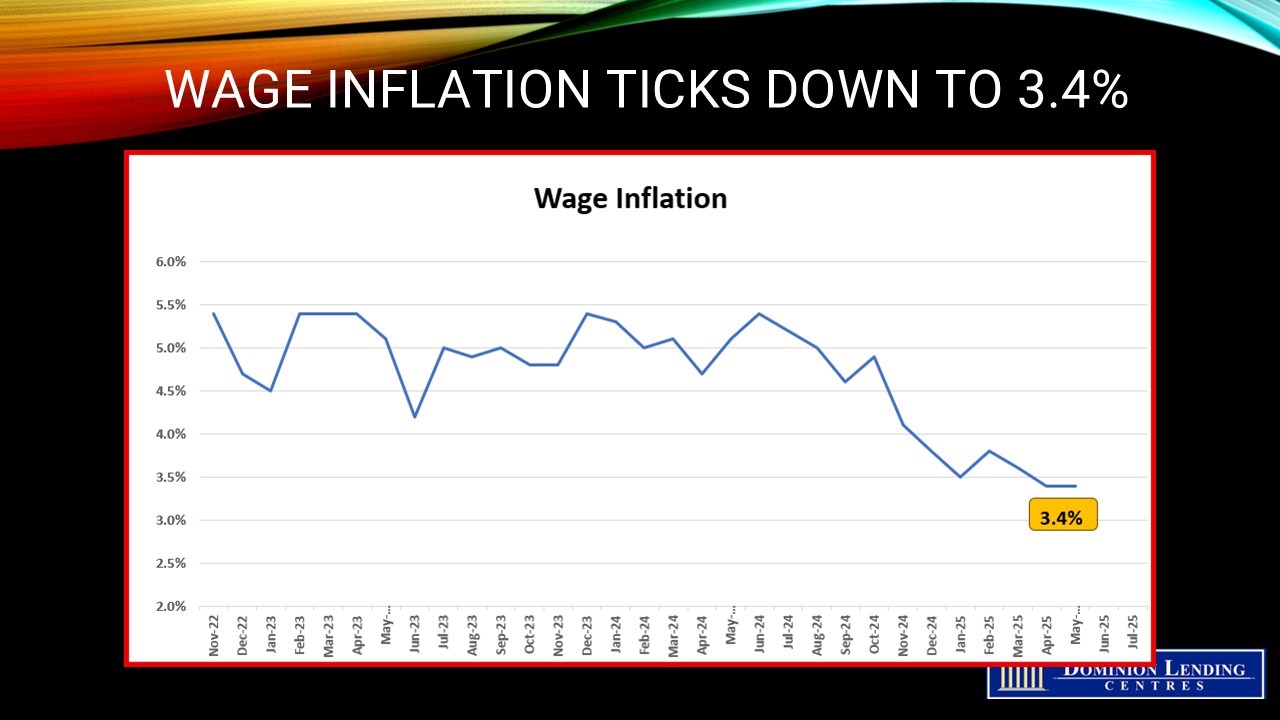

Average hourly wages among employees increased 3.4% (+$1.20 to $36.14) year-over-year in May, the same growth rate as in April (not seasonally adjusted).

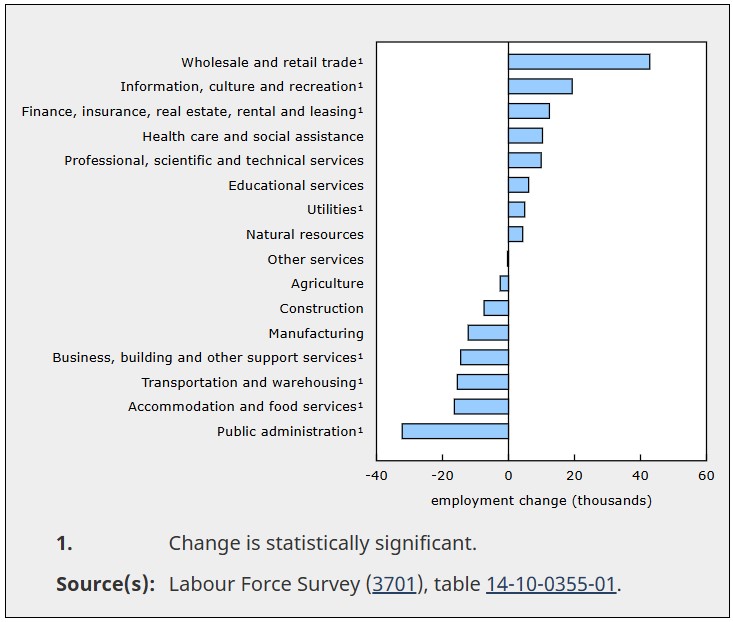

Employment rose in wholesale and retail trade (+43,000; +1.5%) in May, driven by gains in wholesale trade. The increase partially offsets monthly declines in March and April 2025, totalling 55,000 (-1.8%).

In May, employment increased in information, culture and recreation (+19,000; +2.3%) and finance, insurance, real estate, rental and leasing (+12,000; +0.8%). Employment has increased in finance, insurance, real estate, rental and leasing since October 2024, with a net increase of 79,000 (+5.6%) over the period. Meanwhile, public administration employment fell (-32,000; -2.5%), offsetting the increase in April that was related to temporary hiring for the federal election. Prior to these offsetting changes, there had been little change in public administration employment since July 2024.

Chart 5 Employment change by industry, May 2025

Employment also declined in May in transportation and warehousing (-16,000; -1.4%); accommodation and food services (-16,000; -1.4%), and business, building and other support services (-15,000; -2.1%).

Bottom Line

US nonfarm payroll data were released this morning, showing a still resilient economy with tariffs beginning to leave their mark. The US added 139,000 jobs in May, exceeding estimates, while the jobless rate remained at 4.2%. A decline in the labour force participation rate kept the lid on May’s US unemployment rate. But the number of unemployed rose for a fourth month, the longest such streak since 2009. Payrolls for the prior two months were revised downward, and wage gains outstripped inflation, helping to boost consumer spending.

A number of other labour market indicators show signs of increasing stress. Household employment dropped by a whopping 696k in May as the labour force shrank by 625k. This kept the unemployment rate relatively stable at 4.244%, but it is hardly a sign of labour market strength and resilience.

Manufacturing employment dropped by 8k, the sector’s worst performance since January. Construction employment growth also slowed to 4k from 7k in April, which is unusual during the Spring home-selling season. There were also stinging net job losses coming from temporary help firms, retail trade, and the Federal government. These sectors likely feel the combined strain from tariffs and DOGE-driven Federal spending cuts.

Nothing in the May employment report will push the Fed off the sidelines earlier than the markets expect. The steady unemployment rate and improvement in the three-month average of monthly job gains will keep the Fed firmly in the wait-and-see camp. With that said, cracks in the façade of labour market resilience are now starting to show, and the longer the tariff uncertainty and government spending cuts continue, the worse the labour market reports are bound to be. Signs of net job loss in manufacturing, temporary help, retail trade, and government are tell-tale signs of that damage.

On the Canadian side, tariffs have already had a substantial effect on the labour market. The jobless rate is at its highest since 2016, excluding the pandemic, as industries impacted by tariffs are laying off workers. The doubling of the tariff on steel and aluminum is especially deleterious. Trade-related sectors are struggling, while domestic-facing industries are partially offsetting the damage. The May jobs report could have been worse, given that it was burdened by the loss of more than 30,000 election workers. Any increase is welcome, and the gains in private-sector and full-time jobs are encouraging. The glaring issue is that the manufacturing sector is under intense strain amid the deep trade uncertainty, and the overall job market continues to soften, highlighted by the grinding rise in the unemployment rate. In over two years, the jobless rate has risen by two percentage points, as we have gone from 2022 to 2023, when it was difficult to find workers, to today, when it is difficult to find work. While May’s mixed report doesn’t give a clear-cut signal to the BoC, the bigger trend of a rising jobless rate will keep them in easing mode through the year’s second half.

June 22, 2026

Canadian Inflation Rises to Highest Level Since 2023 on the Back of a Spike in Gasoline Prices

June 16, 2026

National home sales jumped 5.5% m/m in May as new listings edged down and the Home Price Index (HPI) was down a meagre 0.1% m/m.

June 10, 2026