Articles

Posted on June 16, 2026

National home sales jumped 5.5% m/m in May as new listings edged down and the Home Price Index (HPI) was down a meagre 0.1% m/m.

Housing Market Regains Momentum, Providing a Strong Handoff into Summer

Canada’s housing market gained meaningful momentum in May, with sales posting their strongest monthly increase of the year and leading indicators pointing to further improvement in June. After months of uncertainty, the market appears to be transitioning from stabilization to recovery as lower borrowing costs, easing energy prices, and improved affordability begin to draw buyers back into the market.

As CREA Senior Economist Shaun Cathcart noted, while May marked the first significant increase in headline sales activity in 2026, underlying market conditions have been improving for several months. Buyers and sellers are increasingly finding common ground on pricing, reflected in firmer sale-to-list price ratios, shorter selling times, and a marked slowdown in price declines. These developments suggest that the period of market adjustment is largely behind us and that home prices are beginning to find a floor.

The next phase of the housing cycle may now be taking shape. Pent-up demand, accumulated over the past two years, is starting to intersect with improved affordability and lower home prices, particularly in Ontario and British Columbia, where price corrections have been most pronounced. As confidence gradually returns, this combination could generate a sustained increase in sales activity through the second half of the year.

The single-family home market, where end-user demand remains strong, is leading the market. The condominium sector, particularly smaller investor-oriented units in major urban centres, continues to face headwinds from higher carrying costs, softer rental markets, and diminished investor participation. Even so, as financing conditions improve and excess inventory is absorbed, activity in the condo market should gradually strengthen.

Taken together, stabilizing prices, balanced market conditions, and rising sales suggest that Canada’s housing market is entering a healthier and more sustainable phase. While regional and segment-specific challenges remain, the broader national trend shows the market regaining its footing and building momentum through the summer.

New Listings

New listings declined by 1.0% in May and were down 7.9% from a year earlier, helping keep the national housing market in balance despite still-modest sales activity. Overall, Canada’s housing market can best be described as stable, although conditions vary considerably by region and property type.

Notable pockets of weakness remain in the Greater Toronto Area, Southwestern Ontario, and parts of British Columbia, particularly in the condominium segment. Smaller investor-oriented condos continue to face the greatest challenges. Much of the exceptional demand for these properties during the pandemic years was driven by investors, but that source of demand has weakened considerably. Higher carrying costs, softer rental markets, and slower population growth following significant reductions in immigration targets have all reduced the attractiveness of investment properties.

At the end of May, there were just over 200,000 properties listed for sale across Canadian MLS® Systems on a non-seasonally adjusted basis. That was essentially unchanged from a year earlier and 2.8% below the long-term average for this time of year, suggesting that supply remains relatively well contained at the national level.

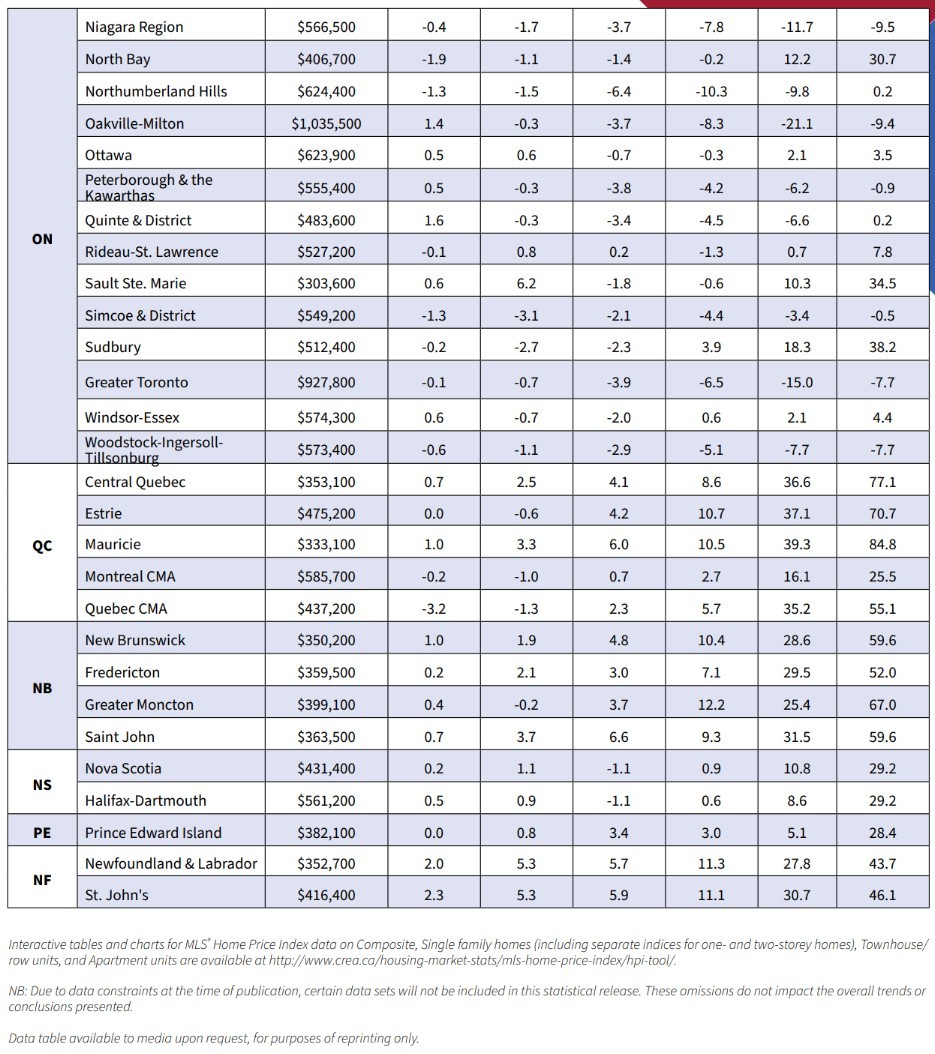

The months-of-inventory measure fell to 4.8 months in May from 5.1 months in each of the previous three months. This is very close to the long-term average of five months and is consistent with a balanced national market. Historically, inventory levels below 3.6 months have signalled seller’s market conditions, while readings above 6.4 months have been associated with buyer’s markets. Taken together, declining new listings, stable inventory, and moderating price declines suggest that Canada’s housing market is gradually finding equilibrium. While certain regions and market segments continue to face adjustment pressures, national conditions have become considerably more balanced than they were earlier in the cycle.

Home Prices

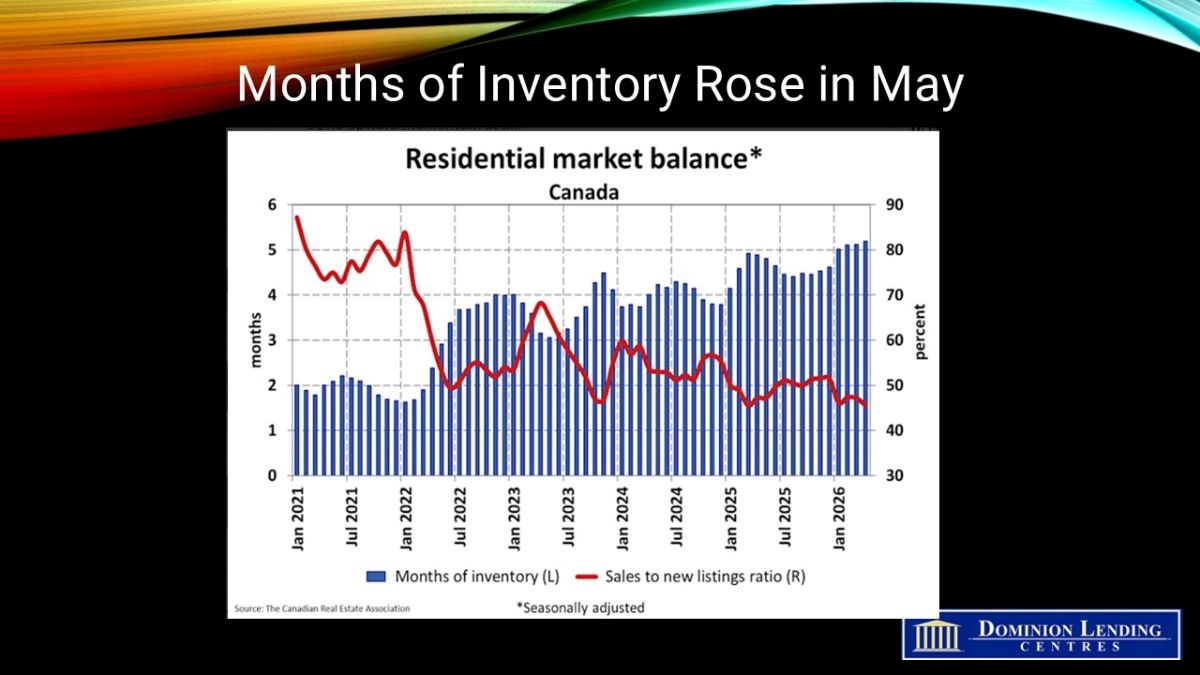

The Canadian housing market continues to show signs of stabilization. In May, the National Composite MLS® Home Price Index (HPI) edged down just 0.1% from April, marking the smallest monthly decline since October 2025. This modest movement is consistent with improving market fundamentals, including firmer sale-to-list price ratios and shorter average days on the market. Stabilizing prices represent an important turning point and could help restore buyer confidence after an extended period of uncertainty.

On a year-over-year basis, the non-seasonally adjusted National Composite MLS® HPI was down 4.2% from May 2025. While still negative, this was the smallest annual decline recorded so far in 2026, suggesting that downward price pressures are gradually easing.

Supply conditions also remain balanced. At the end of May, just over 200,000 properties were listed for sale across Canadian MLS® Systems, virtually unchanged from a year earlier and 2.8% below the long-term average for this time of year.

Taken together, moderating price declines, stable listings, and inventory levels near historical norms suggest that housing market conditions are becoming less challenging for both buyers and sellers. As confidence improves and borrowing costs continue to ease, sales activity could strengthen further in the second half of the year.

Bottom Line

Potential homebuyers faced a challenging backdrop in May as oil prices and interest rates moved higher. Conditions appear more favourable heading into June. News that the Strait of Hormuz is expected to reopen, combined with falling oil prices and easing bond yields, should provide support for housing activity. If a broader agreement between the United States and Iran is reached in the coming weeks, oil prices could decline further, reducing inflation concerns and removing an important headwind for home sales.

The Bank of Canada’s next policy decision is scheduled for July 15. Before then, policymakers will receive several key economic reports, including the May Consumer Price Index (CPI) data and the May Labour Force Survey. Assuming geopolitical tensions continue to ease and energy markets stabilize, the Bank is likely to continue looking through temporary price pressures rather than responding to short-term fluctuations in inflation.

Inflation remains the key risk. Recent U.S. inflation data came in stronger than expected, raising concerns that price pressures could prove more persistent than anticipated. If upcoming Canadian CPI data were to show a similar acceleration, the Bank of Canada would have to consider whether current policy settings remain sufficiently restrictive. While weakness in the labour market and soft housing activity argue against additional tightening, it might be considered, but is likely to be dismissed..

Globally, central banks remain divided. Japan, Norway, and Australia have recently raised interest rates, while the Federal Reserve, the European Central Bank, the Bank of England, and the Bank of Canada all cut rates during 2025 and have remained on hold so far this year. The minutes from the Bank of Canada’s April 29 meeting underscore the Governing Council’s concern about inflation. Policymakers seriously debated the possibility of a rate hike before ultimately deciding to leave rates unchanged. The close nature of that decision highlights the Bank’s continued vigilance and suggests that inflation developments will remain one primary driver of monetary policy in the months ahead. The other driver is economic weakness, which will likely keep the central bank on hold for the remainder of this year.