Articles

Posted on July 15, 2026

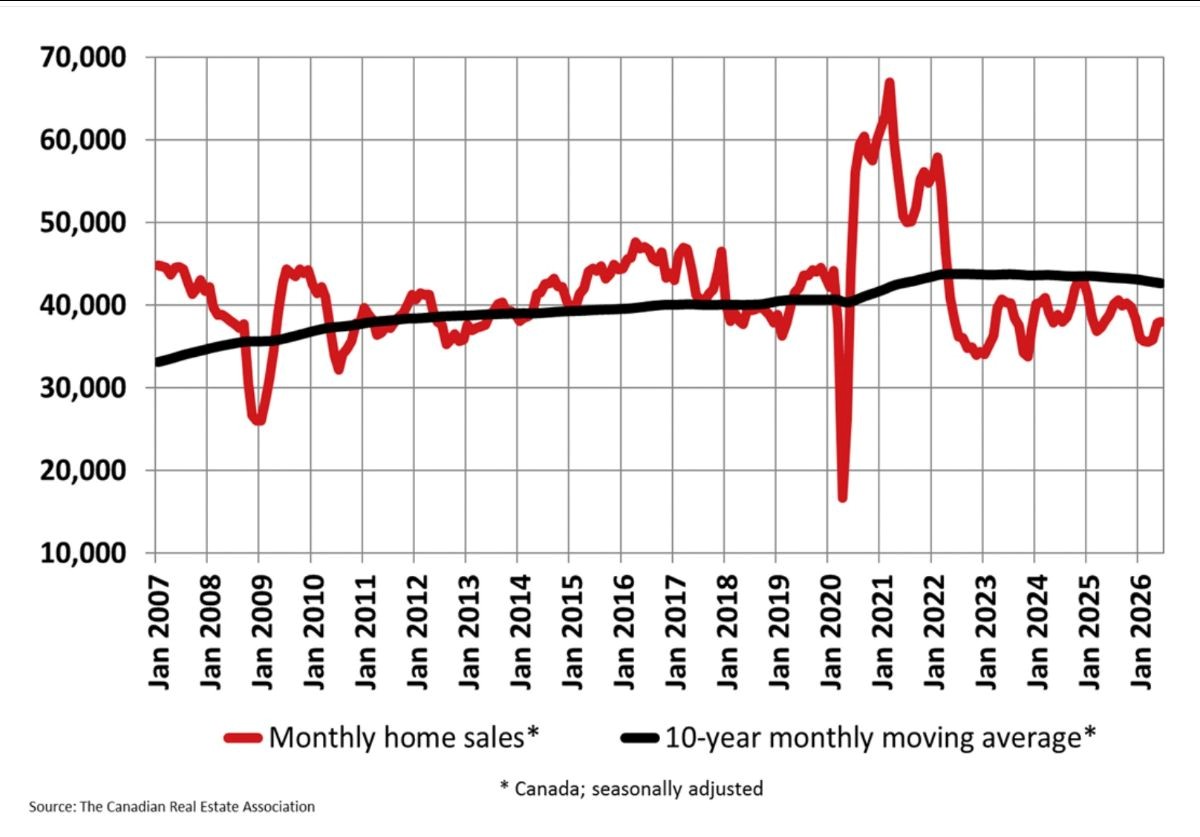

The number of Home Sales Rose a Further 0.5% m/m in June, building on the 5.5% jump in May.

Housing Market Momentum Persists in June, and the Bank of Canada Held Rates Steady

Canada’s housing market gained meaningful momentum in May and June. The number of home sales recorded over Canadian MLS® Systems edged up a further 0.5% on a month-over-month basis in June 2026. This builds on the 5.5% jump recorded in May and the 0.9% increase in April, placing national activity some 7% above its March level.

As CREA Senior Economist Shaun Cathcart noted, while May and June marked the first significant increases in headline sales activity in 2026, underlying market conditions have been improving for several months. Buyers and sellers are increasingly finding common ground on pricing, reflected in firmer sale-to-list price ratios, shorter selling times, and a marked slowdown in price declines. These developments suggest that the period of market adjustment is largely behind us and that home prices are beginning to find a floor.

In other news, the Bank of Canada announced this morning that it would hold the overnight rate steady at 2.25% for the sixth consecutive time. The press release stated that Canada’s economy was showing signs of improvement and inflation is projected to ease gradually from its recent spike. There are still important risks and uncertainties related to the war in the Middle East and US trade policy.

The bottoming in home prices is far more evident in single-family homes than condos, which are still in excess supply, especially in Ontario, which has suffered a marked decline in population with the ouster of many temporary workers and international students and the decline in new permanent residents. The hardest hit have been the steel and aluminum sectors, forest products, and automobiles–all subject to sizable US tariffs.

Since the BoC’s April Monetary Policy Report (MPR), global economic prospects have been dented by higher oil prices stemming from the Middle East conflict. At the same time, the development of artificial intelligence (AI) is supporting economic activity in an increasing number of countries. Oil prices are still below their April peak, but the situation in the Middle East remains volatile. The path of global inflation depends heavily on how the conflict unfolds.

The central bank added that financial conditions in Canada have eased since April and global equity markets have been buoyant. US bond yields have risen, while those in Canada are little changed. This differential has contributed to the depreciation of the Canadian dollar.

Governing Council went on to say that “financial conditions in Canada have eased since April and global equity markets have been buoyant. US bond yields have risen, while those in Canada are little changed. This differential has contributed to the depreciation of the Canadian dollar.”

“Following GDP growth of 0.7% in 2026, the Bank projects the economy will grow by 1.8% in both 2027 and 2028. As the recovery proceeds, economic slack will be gradually absorbed.

CPI inflation rose further to 3.2% in May, mainly because of higher gasoline prices linked to the war in the Middle East. Excluding gasoline, inflation was 2.2%, and measures of core inflation remained near 2%. Near-term inflation expectations are sensitive to changes in gasoline prices, but longer-term inflation expectations remain well anchored. War-related cost pressures are still working their way through some consumer prices but are being offset by downward pressure on other prices from continued economic slack. CPI inflation is expected to remain elevated in June and then ease gradually in the coming months, returning to around 2% in early 2027, although this forecast depends on the path of oil and gasoline prices. Inflation is forecast to average around 2% in 2027 and 2028, albeit with some monthly fluctuations because of base-year effects.

Governing Council judges the current policy rate remains appropriate to sustain the economic recovery and bring inflation back to the 2% target, in line with the MPR projections. Uncertainty is still high. Governing Council will continue to assess the strength of the Canadian economy and the outlook for inflation, and is prepared to adjust monetary policy as needed. The Bank is committed to maintaining Canadians’ confidence in price stability through this period of global upheaval.

Pent-up demand for housing, accumulated over the past two years, is starting to intersect with improved affordability and lower home prices, particularly in Ontario and British Columbia, where price corrections have been most pronounced. As confidence gradually returns, this combination could generate a sustained increase in sales activity through the second half of the year.

The single-family home market, where end-user demand remains strong, is leading the market. The condominium sector, particularly smaller investor-oriented units in major urban centres, continues to face headwinds from higher carrying costs, softer rental markets, and diminished investor participation. Even so, as financing conditions improve and excess inventory is absorbed, activity in the condo market should gradually strengthen. Taken together, stabilizing prices, balanced market conditions, and rising sales suggest that Canada’s housing market is entering a healthier and more sustainable phase. While regional and segment-specific challenges remain, the broader national trend shows the market regaining its footing and building momentum through the summer.

New Listings

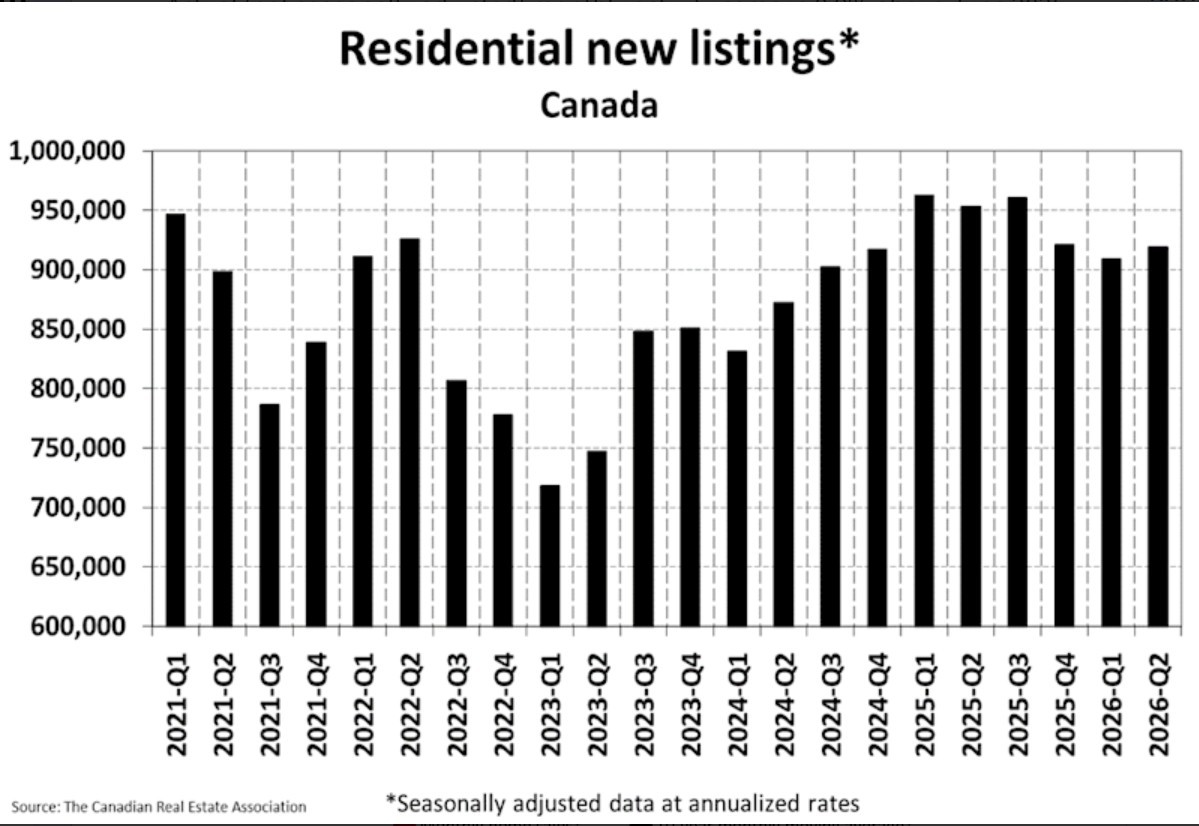

New listings fell back 1.3% on a month-over-month basis in June 2026, marking a second straight decline.

There were 208,578 properties listed for sale on all Canadian MLS® Systems at the end of June 2026, up just 0.6% from a year earlier and 0.8% above the long-term average for that time of the year.

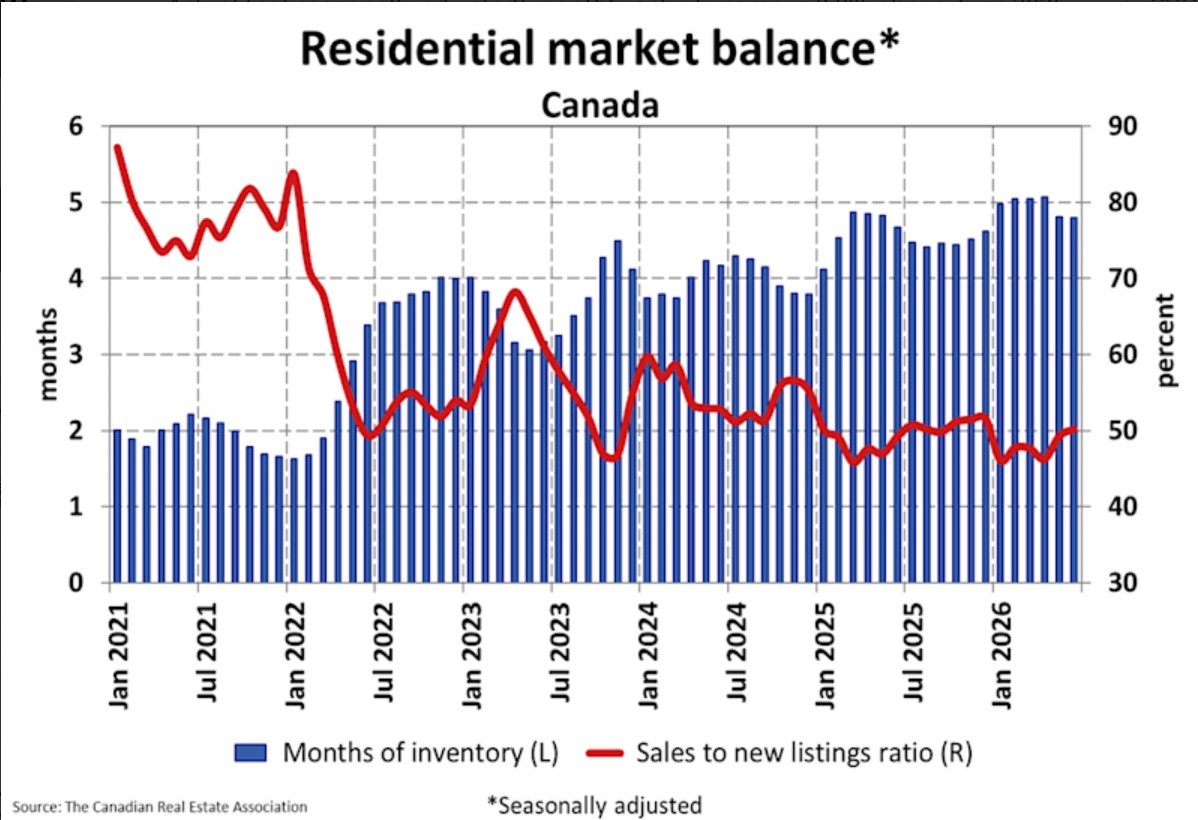

There were 4.8 months of inventory nationally at the end of June 2026, unchanged from May, and the lowest level so far in 2026. This remains close to but slightly below the long-term average for this five-month measure. Based on one standard deviation above and below that long-term average, a sellers’ market would be below 3.6 months, and a buyers’ market would be above 6.4 months.

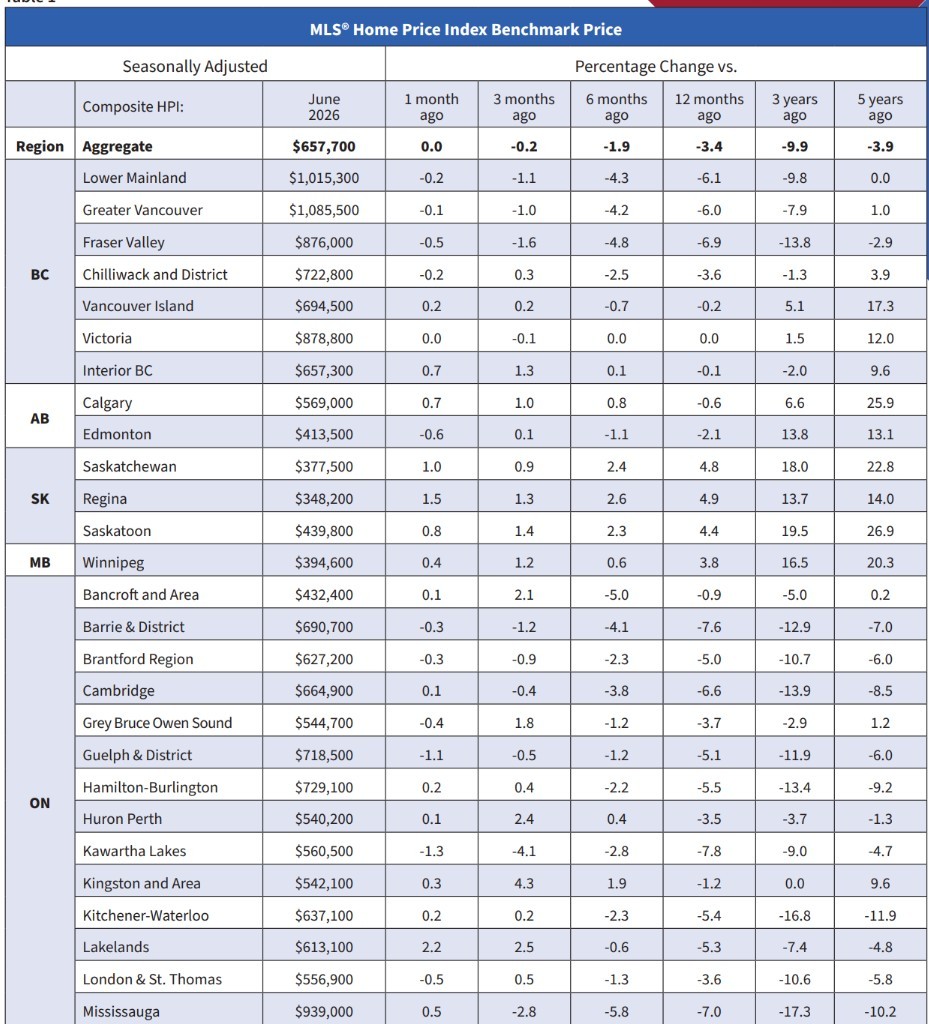

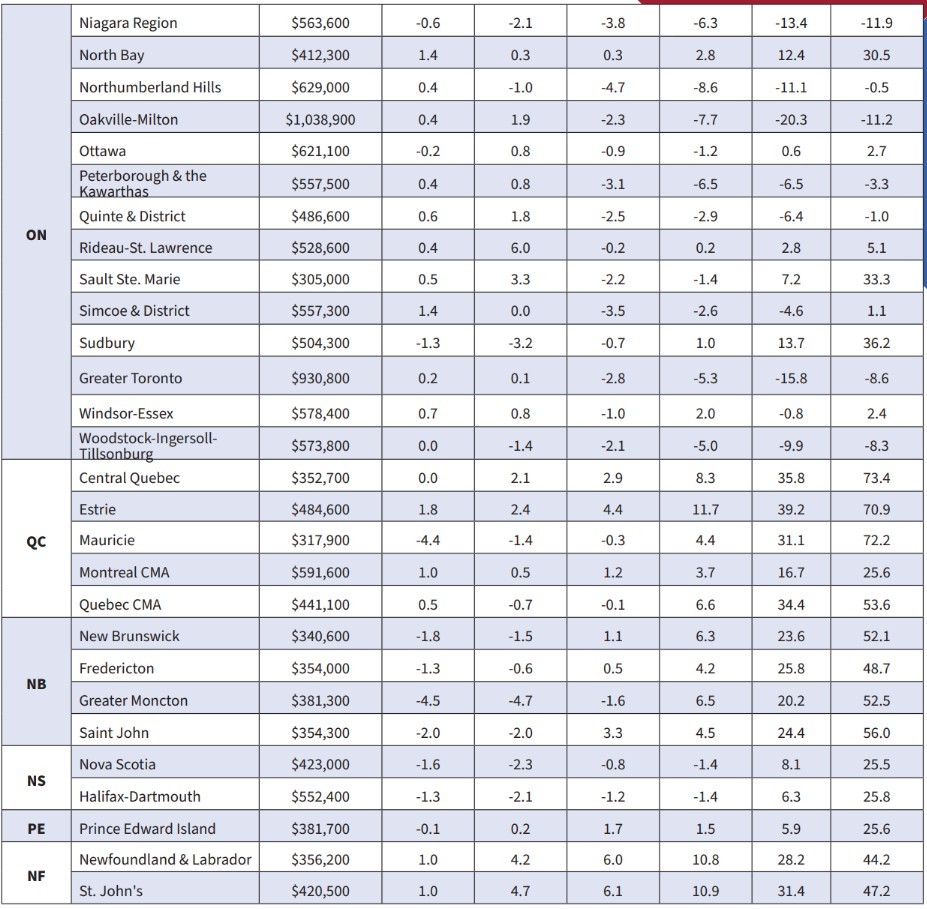

Home Prices

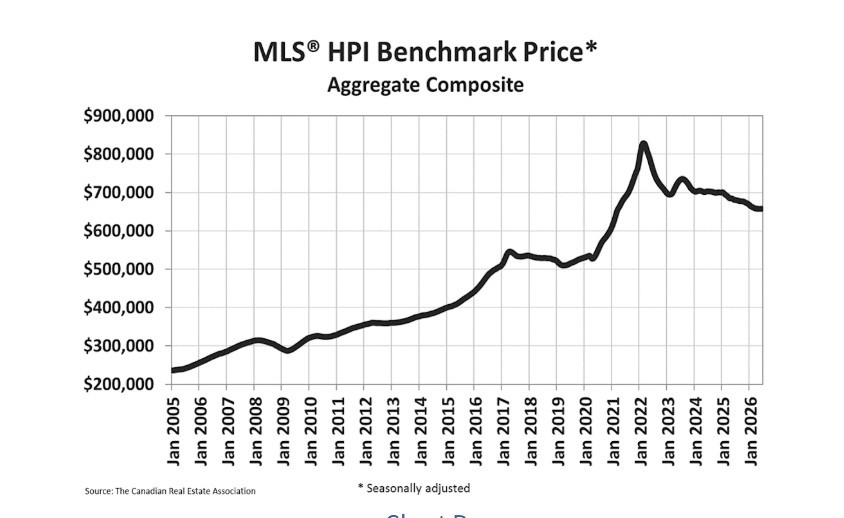

The National Composite MLS® Home Price Index (HPI) held steady from May to June, marking the first time the measure has not declined month over month since January 2025.

Taken together, moderating price declines, stable listings, and inventory levels near historical norms suggest that housing market conditions are becoming less challenging for both buyers and sellers. As confidence improves and borrowing costs continue to ease, sales activity could strengthen further in the second half of the year.

Bottom Line

The brief opening of the Strait of Hormuz triggered a sharp decline in oil prices and market-driven interest rates. Alas, the opening was short-lived as the war resumed in spades. So far, oil price increases have been muted, but uncertainty abounds. President Trump vows to escalate attacks until Iran relents on Hormuz.

US CPI inflation data for June were released this week, showing a decline in month-over-month inflation. Treasuries rose after a report on producer prices reinforced optimism that US inflation has peaked and may curb the need for the Federal Reserve to raise interest rates. The Treasury market had its best day in three weeks Tuesday after a report on consumer prices showed more deceleration than economists had estimated.

The rally trimmed yields across maturities by as much as three to four basis points for short-dated tenors, which are more sensitive to Fed rate adjustments.

We concur with economists surveyed by Bloomberg who expect the Bank of Canada to hold rates at the current level for the rest of the year.

July 15, 2026

The number of Home Sales Rose a Further 0.5% m/m in June, building on the 5.5% jump in May.

June 22, 2026

Canadian Inflation Rises to Highest Level Since 2023 on the Back of a Spike in Gasoline Prices

June 16, 2026