Articles

Posted on July 30, 2025

Bank of Canada Holds Rates Steady as Tariff Clouds Linger

Bank of Canada Holds Rates Steady As Tariff Turmoil Continues

As expected, the Bank of Canada held its benchmark interest rate unchanged at 2.75% at today’s meeting, the third consecutive rate hold since the Bank cut overnight rates seven times in the past year. The Governing Council noted that the unpredictability of the magnitude and duration of tariffs posed downside risks to growth and lifted inflation expectations, warranting caution regarding the continuation of monetary easing.

Trade negotiations between Canada and the United States are ongoing, and US trade policy remains unpredictable.

While US tariffs are disrupting trade, Canada’s economy is showing some resilience so far. Several surveys suggest consumer and business sentiment is still low, but has improved. In the labour market, we are seeing job losses in the sectors that rely on US trade, but employment is growing in other parts of the economy. The unemployment rate has moved up modestly to 6.9%.

Inflation is close to the BoC’s 2% target, but evidence of underlying inflation pressures continues. “CPI inflation has been pulled down by the elimination of the carbon tax and is just below 2%. However, a range of indicators suggests underlying inflation has increased from around 2% in the second half of last year to roughly 2½% more recently. This largely reflects an increase in prices for goods other than energy. Shelter cost inflation remains the biggest contributor to CPI inflation, but it continues to ease. Surveys indicate businesses’ inflation expectations have fallen back after rising in the first quarter, while consumers’ expectations have not come down”.

The Bank asserted today that there are reasons to think that the recent increase in underlying inflation will gradually unwind. The Canadian dollar has appreciated, which reduces import costs. Growth in unit labour costs has moderated, and the economy is in excess supply. At the same time, tariffs impose new direct costs, which will be gradually passed through to consumers. In the current tariff scenario, upside and downside pressures roughly balance out, so inflation remains close to 2%.

The central bank provided alternative scenarios for the economic outlook. In the de-escalation scenario, lower tariffs improve growth and reduce the direct cost pressures on inflation. In the escalation scenario, higher tariffs weaken the economy and increase direct cost pressures.

So far, the global economic consequences of US trade policy have been less severe than feared. US tariffs have disrupted trade in significant economies, and this is slowing global growth, but by less than many anticipated. While growth in the US economy looks to be moderating, the labour market has remained solid. And in China, lower exports to the United States have largely been replaced with stronger exports to other countries.

In Canada, we experienced robust growth in the first quarter of 2025, primarily due to firms rushing to get ahead of tariffs. In the second quarter, the economy looks to have contracted, as exports to the United States fell sharply—both as payback for the pull-forward and because tariffs are dampening US demand.

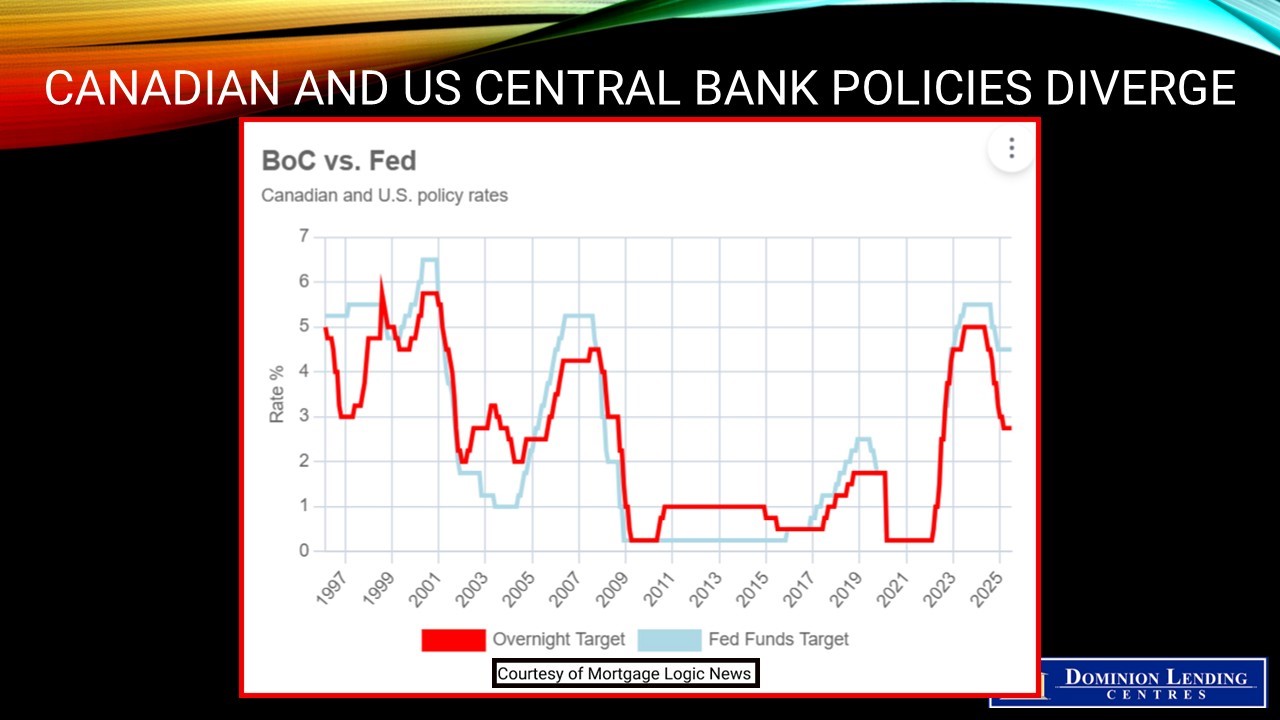

The gap between the 2.75% overnight policy rate in Canada and the 4.25-4.50% policy rate in the US is historically wide. Another cause of uncertainty is the fiscal response to today’s economic challenges. The One Big Beautiful Bill has passed, and it will add roughly US$4 trillion to the already burgeoning US federal government’s red ink. This has caused a year-to-date rise in longer-term bond yields, steepening the yield curve.

The slowdown of the housing sector since Trump’s inauguration has been a substantial drain on the economy. The Monetary Policy Report (MPR) for July states that “growth in residential investment strengthens in the second half of 2025, partially due to an increase in resale activity after the steep decline in the first half of the year. Growth in residential investment is moderate over 2026 and 2027, supported by dissipating trade uncertainty and rising household incomes.”

Bottom Line

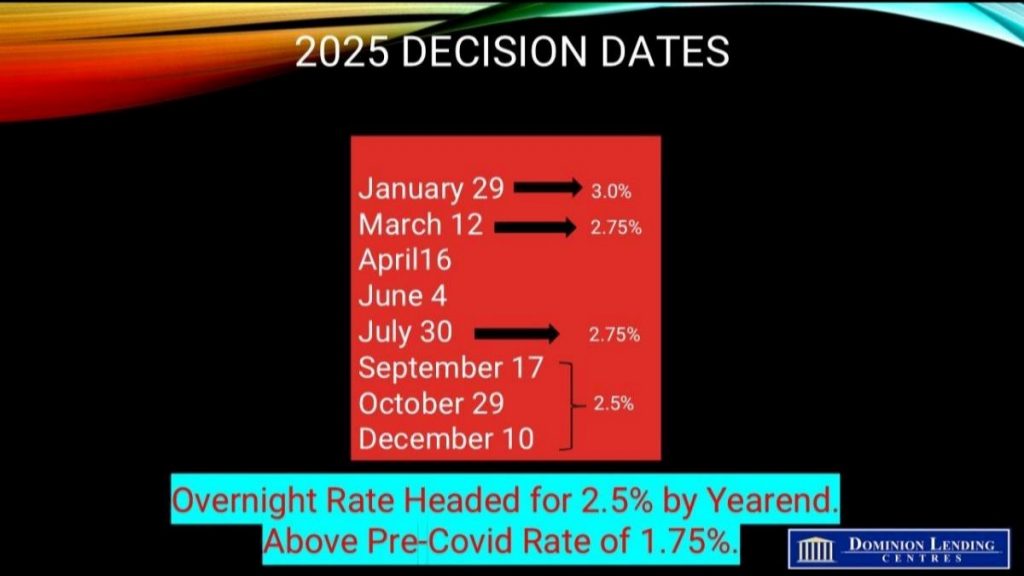

We expect the Canadian economy to post a small negative reading (-0.8%) in Q2 and (-0.3%) in Q3, bringing growth for the year to 1.2%. The next Governing Council decision date is September 17, which will give the Bank time to assess the underlying momentum in inflation and the dampening effect of tariffs on economic activity.

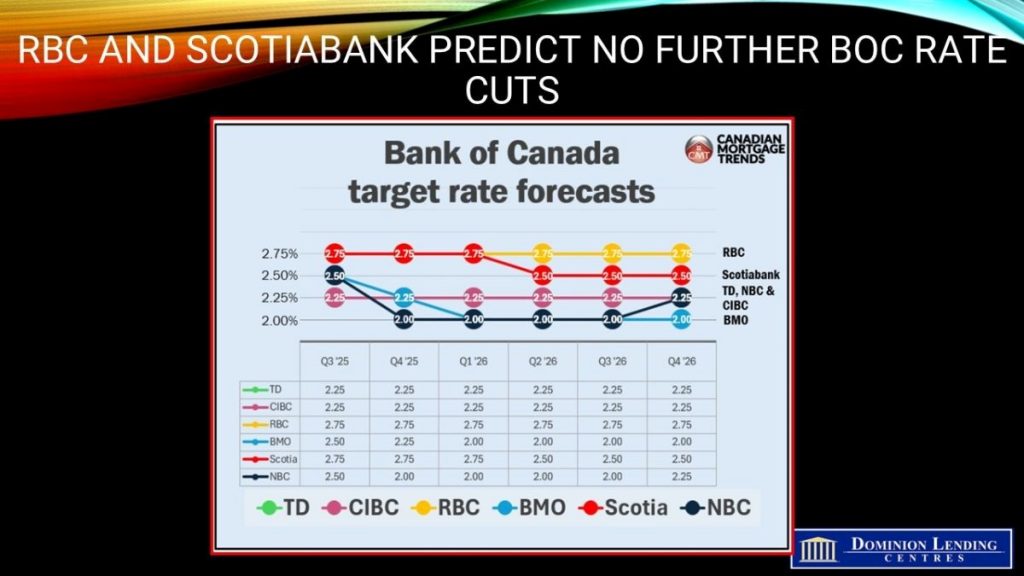

If inflation slows over the next couple of months and the economy slows in Q2 and Q3 as widely expected, the Bank will likely cut rates one more time this year, bringing the overnight rate down to 2.50%, within the neutral range for monetary policy. Bay Street economists have varying views on the rate outlook (see chart above). While the Fed will hold rates steady today, despite the incredible pressure coming from the White House, the Bank of Canada could well cut rates one more time this year.