Articles

Posted on January 16, 2023

Canadian Existing Home Sales Fell by a Record 25% in 2022

December Housing Data Ended 2022 On A Weak Note

Statistics released today by the Canadian Real Estate Association (CREA) show national home sales were up month-over-month in December while new listings plummeted and national home prices fell again.

Home sales recorded over Canadian MLS® Systems increased 1.3% between November and December 2022. Ottawa and Edmonton led gains. Nevertheless, the actual number of transactions last month was 39.1% below year-ago levels and dramatically below the 10-year monthly moving average for December (see chart below).

New Listings

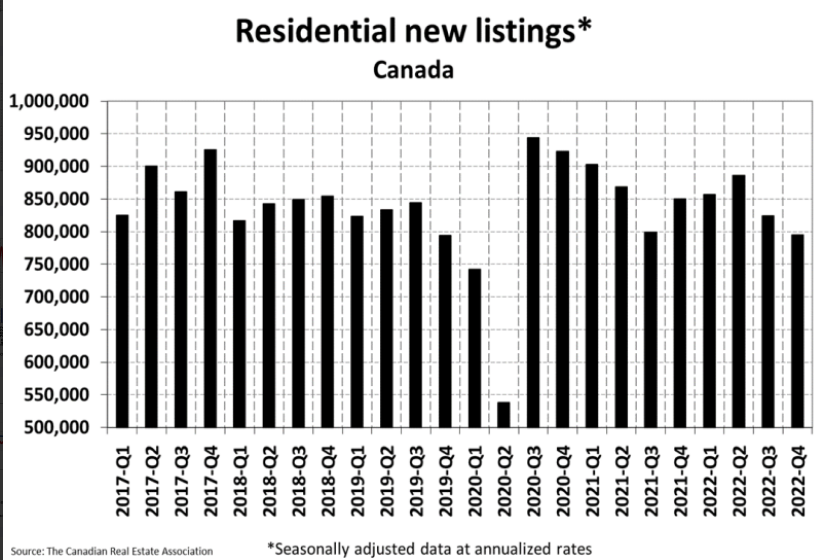

Sellers remained on the sidelines. The number of newly listed homes dropped 6.4% month-over-month in December, led by British Columbia and Quebec declines. It was among the lowest December new supply levels on record.

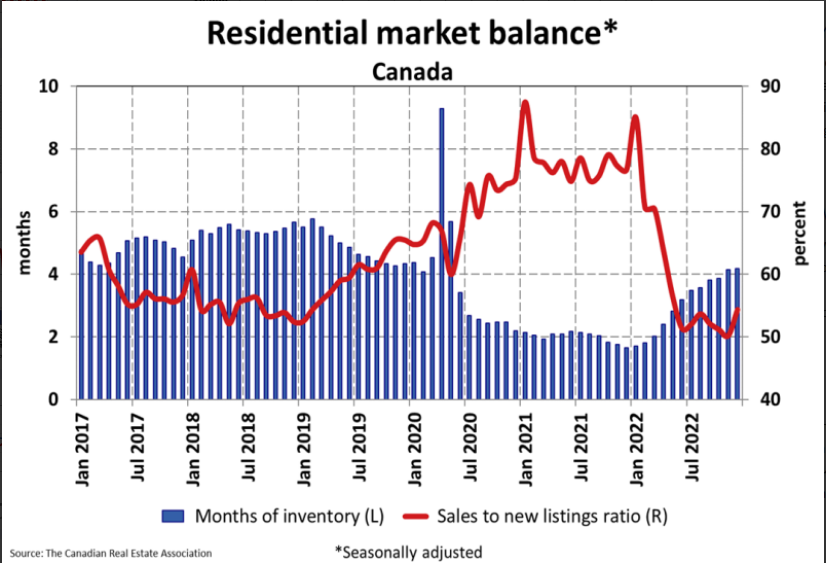

With new listings down by quite a bit more than sales on a month-over-month basis, the sales-to-new listings ratio tightened to 54.4% compared to 50.2% posted in November. The long-term average for this measure is 55.1%.

There were 4.2 months of inventory on a national basis at the end of December 2022. This is close to where this measure was in the months leading up to the initial COVID-19 lockdowns and still nearly a full month below its long-term average.

Home Prices

Canadian home prices fell by the most on record in 2022 as rapidly rising interest rates forced a market adjustment that may not yet be over. The country’s benchmark home price fell 1.6% in December to C$730,600, bringing the total decrease since March to 16.4%. Last year also saw the most significant price decline for a calendar year since records began, with a 7.5% drop overall.

The Aggregate Composite MLS® HPI, which adjusts for the type of property sold, now sits about 13% below its peak level. Looking across the country, prices are down more than they are nationally in Ontario and parts of B.C. and down by less elsewhere. While prices have softened to some degree almost everywhere, Calgary, Regina, Saskatoon, and St. John’s stand out as markets where home prices are barely off their peaks at all.

The non-seasonally adjusted Aggregate Composite MLS® HPI was 7.5% below its December 2021 reading.

The table below shows the decline in MLS-HPI benchmark home prices in Canada and selected cities since prices peaked in March when the Bank of Canada began hiking interest rates. More details follow in the second table below. The most significant price dips are in the GTA and the GVA, where the price gains were spectacular during the Covid-shutdown.

Even with these large declines, prices remain roughly 33% above pre-pandemic levels.

Bottom Line

Tomorrow, we will see the release of the Canadian CPI data for December. I expect a continued improvement in the headline and core inflation rates. Even so, the odds favour a 25 bps hike in the overnight policy rate next week when the Bank of Canada announces its decision. Labour data for December remained strong; the economy has shown continued resilience, and today’s Business Outlook Survey deteriorated further in the fourth quarter.

Inflation expectations remain elevated as the share of firms expecting inflation to be above 3% over the next year hit a new record high of 84%. Almost 40% of respondents expect inflation to persist well above 2% into 2026 and beyond, reflecting perceived stickiness in energy prices, supply chain issues, strong demand, and labour costs, as well as the time it takes for monetary policy to slow inflation.

In a separate release, the BoC’s Survey of Consumer Expectations showed that consumers feel the pinch of reduced purchasing power and increasing wage demands. One-year-ahead inflation expectations remained elevated at over 7%, though expectations moderated at longer time horizons.

July 21, 2026

The US Announces a 50% tariff on a wide array of goods that are covered under CUSMA effective August 19

July 15, 2026

The number of Home Sales Rose a Further 0.5% m/m in June, building on the 5.5% jump in May.

June 22, 2026