Articles

Posted on February 15, 2017

New Mortgage Regulations Weigh On Home Sales

This morning, the Canadian Real Estate Association (CREA) released its January national real estate statistics showing home sales declined 1.3% month-over-month in the first month of this year. This down draft put resales at their second lowest monthly level since the fall of 2015 and only a bit above levels recorded last November when new tighter mortgage regulations were first put in place.

Activity was down in about 50% of all local markets, led by the three largest urban markets–The Greater Toronto Area (GTA), Greater Vancouver and Montreal.

For the year as a whole, the number of homes changing hands was up 1.9%. Sales slowed in the second half of 2016 and the newly released data show that the slowdown continues. Notably, year-over-year sales were down significantly in the Lower Mainland of British Columbia (BC). This slowdown was exacerbated by the August introduction of the 15% land transfer tax on foreign nonresident purchasers. The October tightening of mortgage regulations dampened activity further.

Housing activity will not provide the boost to overall economic growth in 2017 that it did in 2015 and the first half of 2016. as first-time homebuyers will find it more difficult to qualify for a mortgage and credit availability is diminished by the disproportionate impact of the new regulations on nonbank lenders.

Sales activity was down from the previous month in about half of all local markets, led by three of Canada’s largest urban centres: the Greater Toronto Area (GTA), Greater Vancouver and Montreal.

Supply shortages are a major issue depressing sales activity and raising prices, especially in and around Toronto and parts of BC. Price pressures will continue in these markets unless demand declines significantly.

New Listings Continue To Decline

The number of newly listed homes fell 6.7% in January, the second consecutive monthly decline. New listings were down in about two-thirds of all local markets, led by the GTA and environs across Vancouver Island.

The monthly decline in new listings dwarfed the decline in sales so the national sales-to-new listings ratio jumped to 67.7% last month compared to 64.0% in December and 60.2% in November. The ratio in the range of 40%-to-60% is considered generally consistent with balanced housing market conditions. Above 60% is considered a sellers’ market and below 40%, a buyers’ market.

The sales-to-new-listings ratio was above 60% in half of all local housing markets again last month–the vast majority of which continued to be in British Columbia, in and around the Greater Toronto Area and across Southwestern Ontario. There were sellers markets already in these regions.

Number of Months of Inventory

The number of months of inventory is another important measure of the balance between housing supply and demand. It represents the number of months it would take to completely liquidate current inventories at the current rate of sales activity.

There were 4.6 months of inventory on a national basis at the end of January–unchanged from December and a six-year low for this measure. Clearly government efforts to increase supply is warranted.

The imbalance between limited housing supply and relatively strong demand in Ontario’s Greater Golden Horseshoe region is without precedent (the region includes the GTA, Hamilton-Burlington, Oakville-Milton, Guelph, Kitchener-Waterloo, Cambridge, Brantford, the Niagara Region, Barrie and nearby cottage country). The number of months of inventory in January is now at or below one month of sales in the GTA, Hamilton-Burlington, Oakville-Milton, Kitchener-Waterloo, Cambridge, Brantford and Guelph.

Prices Continue to Rise

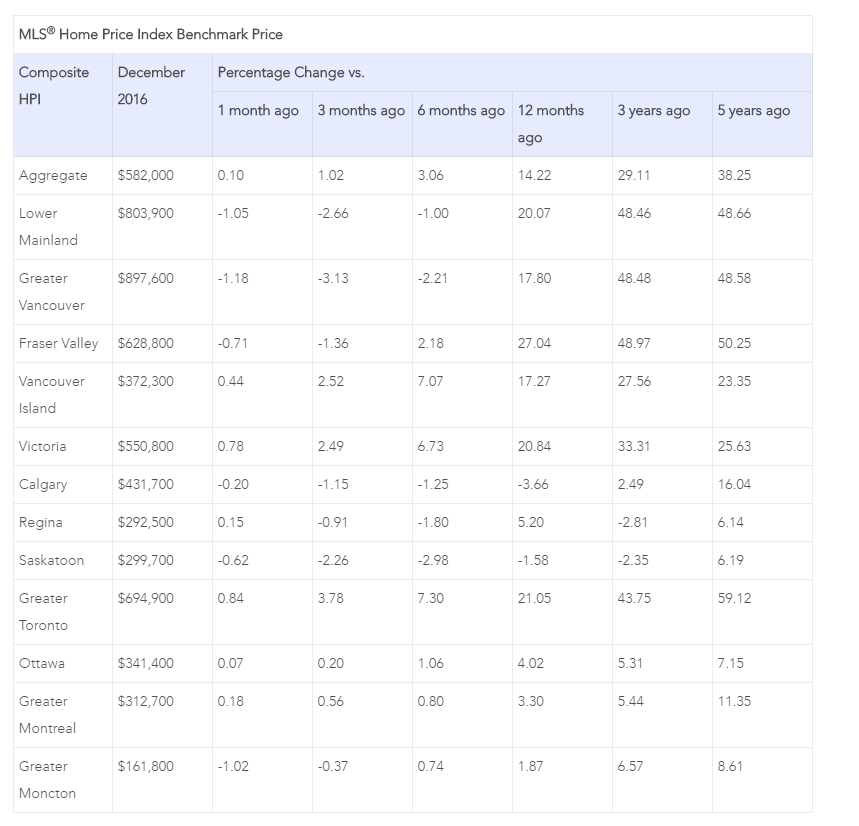

The Aggregate Composite MLS House Price Index (HPI) rose 15.0% y-o-y last month. This was up a bit from December’s gain, reflecting an acceleration in condo and townhouse unit price increases.

This price index, unlike those provided by local real estate boards and other data sources, provides the best gauge of price trends because it corrects for changes in the mix of sales activity (between types and sizes of housing) from one month to the next.

Prices for two-storey single family homes posted the strongest year-over-year gains (+16.8%), followed closely by townhouse/row units (+15.8%), one-storey single family homes (+14.4%) and apartment units (+13.3%). In many of these regions, the supply of new single-family homes is so limited, you practically need to knock down a house to build a new one.

Price trends continued to vary widely by location. In the Fraser Valley and Greater Vancouver, prices continued to recede from their peaks reached in August 2016 but remained above year-ago levels (+24.9% y-o-y and +15.6% y-o-y respectively). Meanwhile, benchmark prices climbed to new heights in Victoria and elsewhere on Vancouver Island as well as in the Oakville-Milton, Guelph, and the GTA. Year-over-year price gains in these five markets ranged from about 18% to 26% in January. By comparison, home prices were down 2.9% y-o-y in Calgary and edged lower by 1.0% y-o-y in Saskatoon, continuing their retreat from peaks reached in 2015. Prices in these two markets are down 5.9% in Calgary and 4.3% in Saskatoon relative to their 2015 peak levels.

Home prices were up modestly from year-ago levels in Regina (+3.8%), Ottawa (+3.7%), Greater Montreal (+3.1%). In Greater Moncton, prices held steady. Monthly trends suggest that prices have continued to stabilize in these markets.

The actual (not seasonally adjusted) national average price for homes sold in January 2017 was $470,253 about in line with where it stood one year earlier. This marks the smallest y-o-y increase in nearly two years.

The national average price continues to be pulled upward by sales activity in Greater Vancouver and the GTA, which remain two of Canada’s tightest, most active and expensive housing markets. That said, Greater Vancouver’s share of national sales activity has diminished considerably over the last year, giving it less upward influence on the national average price. The average price is reduced by almost $120,000 to $351,998 if Greater Vancouver and GTA sales are excluded from calculations.