Articles

Posted on December 6, 2024

November Jobless Rate Surges to 6.8% in Canada Despite Strong Jobs Growth

The Surge In Canadian Unemployment Keeps Another Jumbo Rate Cut In Play In December

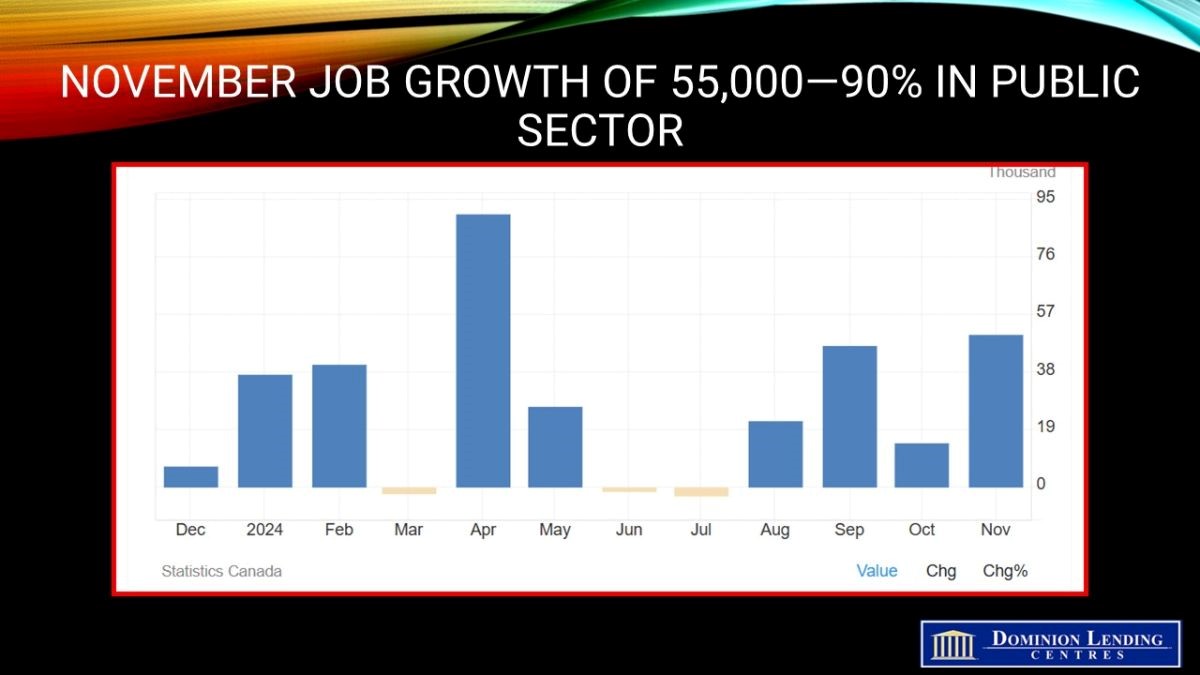

Before the release of today’s Canadian Labour Force Data, the odds favoured a 25 basis point drop in the overnight policy rate when the Bank of Canada meets again on December 11th. The data showed more substantial than expected job creation, as the country added 51,000 net new positions in November compared to the expected rise of 25,000. However, nearly 90% of the job growth was in the public sector, dampening enthusiasm.

Public sector employment rose by 45,000 (+1.0%) in November and accounted for the majority of the overall employment gain in the month. The number of private sector employees and the number of self-employed people were both little changed in November.

The number of public-sector employees grew by 127,000 (+2.9%) in November compared with 12 months earlier. The increase was driven by the public-sector components of health care and social assistance (+81,000) and educational services (+48,000) (not seasonally adjusted). Over the same period, private-sector employment rose at a slower pace (+1.3%; +173,000).

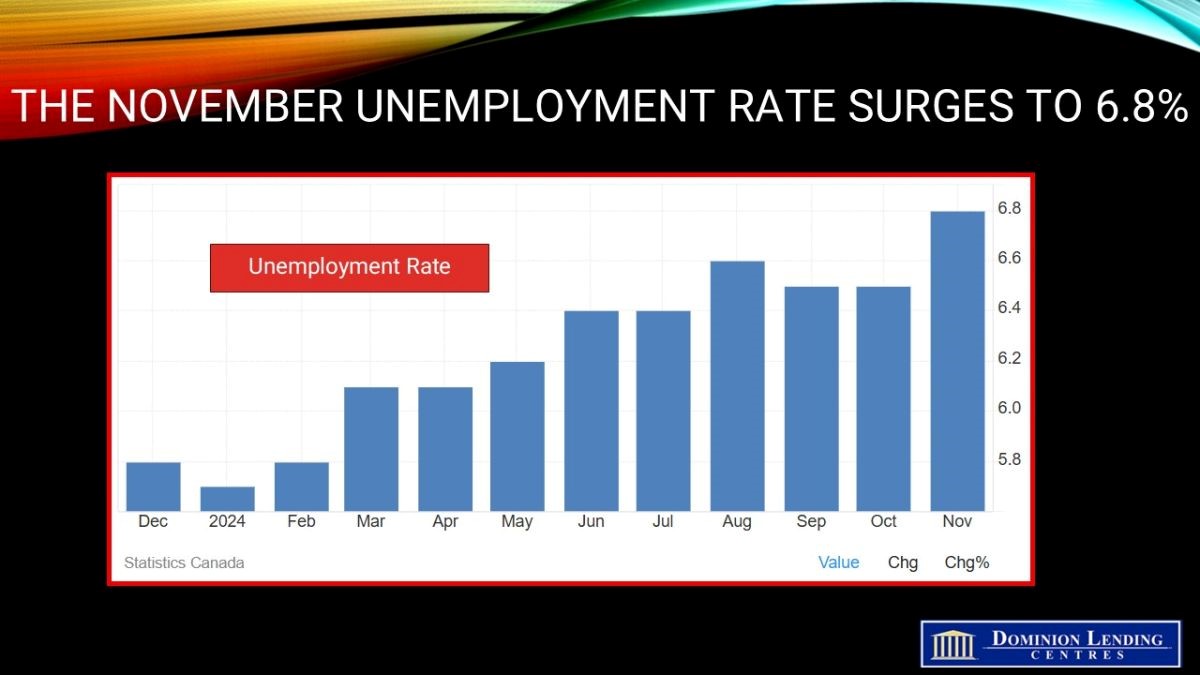

Despite the sharp rise in employment, the jobless rate surged to its highest level in three years, bolstering the case for the BoC to consider another 50 bps rate cut next week. Statistics Canada said Friday that unemployment jumped 0.3 percentage points to 6.8%. The jobless rate is now the highest since January 2017 excluding the pandemic period.

Interest rates fell on the news. Traders in overnight swaps boosted the odds of a 50 basis-point cut at the Bank of Canada’s decision next week at more than three-quarters, from about a coin flip previously. The report was released at the same time as US nonfarm payrolls, which rose by 227,000 while the unemployment rate rose to 4.2%.

The report underscores ongoing labour market softness that had already convinced the Bank of Canada to ramp up the pace of rate cuts with a 50 basis-point reduction in October.

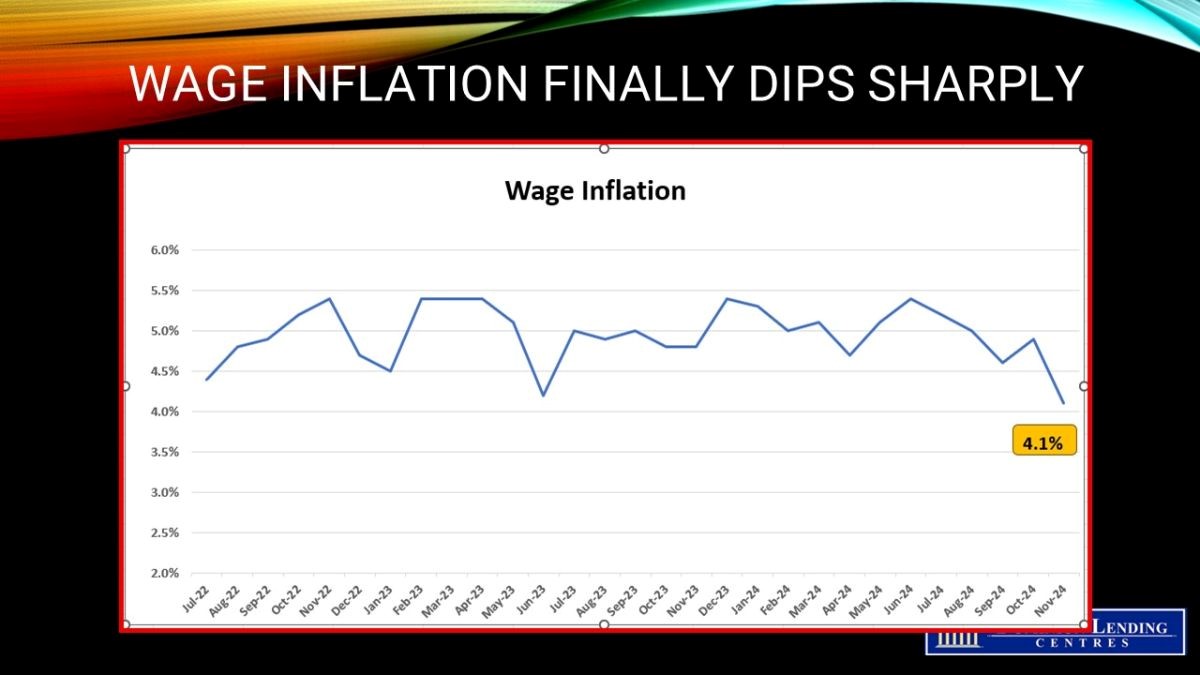

Other details in the report pointed to a slowing economy. Hours worked dipped 0.2%, posting its third decline in the past four months. Also flagging was wage inflation, which cooled considerably. After remaining very strong for months, wage inflation dipped to 4.1% in November, down from 4.9% in October and marking its slowest pace in two years.

After falling for six consecutive months from May to October, the employment rate—the proportion of the population aged 15 and older who are employed—held steady at 60.6% in November. Employment growth in the month kept pace with growth in the population aged 15 and older in the Labour Force Survey (LFS) (+0.2%). On a year-over-year basis, the employment rate was down 1.2 percentage points.

The proportion of long-term unemployed people has increased along with the unemployment rate. In November, 21.7% had been continuously unemployed for 27 weeks or more, up 5.9 percentage points from a year earlier.

The labour force participation rate—the proportion of the population aged 15 and older who were employed or looking for work—increased by 0.3 percentage points to 65.1% in November, offsetting a cumulative decline of 0.3 percentage points in September and October. The participation rate was down by 0.5 percentage points on a year-over-year basis.

Bottom Line

Monetary policy remains overly restrictive as the 3.75% overnight policy rate remains well above the inflation rate. We expect the overnight rate to fall to 2.5% by April or June of next year. This should continue boosting housing activity, which increased significantly in October and November.

Last week’s GDP data release showed that Canada’s third-quarter GDP grew a mere 1.0%, well below the Bank’s downwardly revised forecast of 1.5%. This, in combination with today’s employment report, bodes well for the Bank of Canada to consider cutting rates by another 50 bps seriously. However, given how aggressive they have been compared to the Federal Reserve, which will undoubtedly cut rates by only 25 bps in late December, they could be satisfied with a 25 bp cut for now