Canadian Home Sales and New Listings Plunge in April

Record Declines in Canadian Home Sales and Listings in April

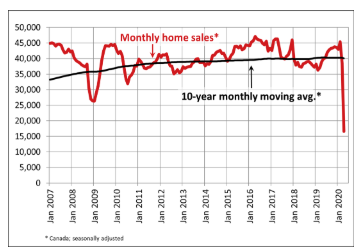

The pandemic shutdown has put every sector of the economy into a medically induced coma, so, of course, the housing sector is no exception. Data released this morning from the Canadian Real Estate Association (CREA) showed national home sales fell a record 56.8% in April, compared to an already depressed March, in the first full month of COVID-19 lockdown (see chart below). Transactions were down across the country.

Among Canada’s largest markets, sales fell by 66.2% in the Greater Toronto Area (GTA), 64.4% in Montreal, 57.9% in Greater Vancouver, 54.8% in the Fraser Valley, 53.1% in Calgary, 46.6% in Edmonton, 42% in Winnipeg, 59.8% in Hamilton-Burlington and 51.5% in Ottawa.

The residential real estate industry is not standing still, however. Technological innovation is creating new ways of buying and selling homes. According to Shaun Cathcart, CREA’s Chief Economist, “Preliminary data for May suggests things may have already started to pick up a bit for both sales and new listings, in line with evidence that realtors and their clients have adopted new and existing virtual technology tools. These tools have allowed quite a bit of essential business to safely continue, and will likely remain key for some time.”

I have heard agents discussing software that virtually “stages” properties, allowing potential buyers to see the possibilities of existing and renovated floor plans and options in decor and design. The software replaces the need for expensive “physical” staging and can be far more creative. Where there is challenge, there is opportunity, and the people that create and adopt these innovative virtual solutions could be big winners.

Keeping the lid on price pressures, the number of newly listed homes across Canada declined by 55.7% m-o-m in April. The Aggregate Composite MLS® Home Price Index declined by only 0.6% last month, the first decline since last May. While some downward pressure on prices is not surprising, the comparatively small change underscores the extent to which the bigger picture is that both buying and selling is currently on pause.

Mortgage Qualifying Rate Set To Drop

The mortgage qualifying rate, the so-called Big Bank posted rate, has been above 5% since the OSFI stress test began on January 1, 2018. Despite dramatic declines in the government of Canada bond yield, which currently hovers at a mere 0.388%, and a huge fall in contract mortgage rates, the banks have kept their posted rates elevated. The minimum stress test rate began in 2018 at 5.34%, then finally fell to 5.19% and more recently to 5.04%–all still at a historically wide margin above market-determined rates.

In the past week, RBC and BMO have cut their 5-year posted rates slightly further to 4.94%. If no other banks follow, the Bank of Canada’s OSFI stress test rate will fall to 4.99%. If at least one other bank goes to 4.94%, the qualifying rate will drop to 4.94%. Every little bit helps.

With the first news of the COVID-19 pandemic threat, the BoC report said that “uncertainty about just how bad things could get created shock waves in financial markets, leading to a widespread flight to cash and difficulty selling assets. Policy actions are working to:

restore market functioning

ensure that financial institutions have adequate liquidity

give Canadian households and businesses access to the credit they need”

The Bank of Canada’s actions have put a floor under the economy. These along with the federal government spending initiatives and the mortgage deferral program have cushioned the blow to households and businesses. Governor Poloz said, “our goal in the short-term is to help Canadian households and businesses bridge the crisis period. Our longer-term goal is to provide a strong foundation for a recovery in jobs and growth.”

With the economic outlook remaining highly uncertain, the BoC erred on the side of caution in projecting mortgage arrears and non-performing business loans based on the more severe economic scenario it laid out in the April Monetary Policy Report. The pessimistic reading would be that even with policymakers’ extraordinary actions, that scenario would see mortgage and business loan delinquencies eclipse previous peaks. A more optimistic reading would be that policy support has prevented a significantly worse outcome, and a resilient financial system will be able to absorb losses and leave the foundation in place for an eventual economic recovery. And, as Governor Poloz mentioned, a better economic scenario is still within reach as many provinces are beginning to gradually re-open their economies.

The projections in today’s FSR are based on a scenario in which Canadian GDP is 30% lower in Q2 and recovers slowly thereafter. In that scenario, mortgage arrears are projected to increase to 0.8% by mid-2021 from 0.25% at the end of 2019–nearly double the peak in arrears seen in 2009. Meanwhile, non-performing business loans are forecast to rise to 6.4% at the end of this year from 1% at the end of last year, significantly higher than past peaks of less than 5% in 2003 and 2010.

The upshot is that while we might see a significant increase in mortgage arrears and troubled loans over the next two years in this pessimistic economic scenario, these outcomes would have been much worse without the extraordinary programs that have been put in place to support businesses and households. That has important implications for the banking sector. The BoC’s analysis suggests that, with these policy measures, large bank’s existing capital buffers should be sufficient to absorb losses. Without those interventions, “banks would be faring much worse, with important negative effects on the availability of credit to households and businesses.”

Households:

1 in 5 households don’t have enough cash or liquid assets to cover two months of mortgage payments

Government support programs (CERB payments and CEWS wage subsidies) will cover a large share of households’ “core” spending (food, shelter, and telecoms)

Loan payment deferrals (banks have allowed more than 700,000 households to delay mortgage payments) and new borrowing can help offset remaining income losses

Still, some households are likely to fall behind on their debt payments (first credit cards and auto loans, then mortgages)—something we’re already seeing in Alberta and Saskatchewan

Businesses:

There have been some signs of reduced funding stress in April: The Bank of Canada’s bankers’ acceptance program is shrinking, the drawdowns of credit lines have slowed as some borrowers are repaying, and corporate debt issuance picked up significantly in April after ceasing in March.

Surveys show higher-than-normal rejection rates for small- and medium-sized businesses requesting additional funding from financial institutions

Upcoming corporate debt refinancing needs are in line with historical levels, but many borrowers will face in increased costs of funds owing to elevated corporate risk spreads

Nearly three-quarters of investment-grade corporate bonds are rated BBB (the lowest investment grade rating)—downgrades would double the stock of high-yield debt and significantly increase funding costs for those borrowers

Firms in the industries most affected by COVID-19 tend to have smaller cash buffers, and a sharp drop in revenues will make it difficult to meet fixed costs including debt payments. What started as a cash flow problem could develop into a solvency issue for some businesses

The energy sector is facing particular challenges: it has had to rely more on credit lines, has the highest refinancing needs over the next six months and faces the most potential downgrades

Banks:

BoC’s term repos have provided ample liquidity to the banking system and reduced funding costs, hence the drop in some banks’ posted and contract mortgage rates

Take-up of term repos has slowed in recent weeks—an indication of improved market functioning

Regulators have eased capital and liquidity requirements

Governments:

The BoC’s asset purchases have helped improve liquidity in the key Government of Canada securities market (the baseline for many other bond markets)

The FSR made little mention of government debt sustainability, but in his press conference Governor Poloz noted that overall government debt levels are similar to 20 years ago, and federal debt is significantly lower, giving the federal government plenty of room to maneuver

Bottom Line:

Of course, the pandemic shutdown has strained the financial wherewithal of many households and businesses. That was deemed the price we must pay to mitigate the severe health threat and contain its spread. The BoC report acknowledges the economic fallout of the necessary measures and promises to take additional actions to assure the economy returns to its full potential growth path as soon as feasibly possible. Cushioning the blow for those most in need.

Nevertheless, there are businesses that will close permanently and others that will scoop up declining competitors. Some will benefit from the new opportunities created by social distancing, enhanced sanitation, remote activity, new forms of entertainment and advances in healthcare. Others will no doubt die, although many of these companies were at death’s door before the pandemic emerged. Creative destruction is always painful for the losers, but it opens the way for many new winners and those existing businesses and individuals that are creative enough to adapt quickly to the changing environment.