Articles

Posted on August 15, 2024

Canadian Housing Market On Pause In July

Canadian Housing Market Paused In July

Despite the continued decline in interest rates, the Canadian housing market saw summer doldrums last month. The Canadian Real Estate Association (CREA) announced today that national home sales fell 0.7% monthly while rising 4.8% from year-ago levels. A significant uptick in sales activity is likely this fall, reflecting both Bank of Canada easing and a dramatic drop in market-driven interest rates. Yesterday, the US CPI dipped below 3.0% y/y, causing a significant bond rally. The five-year government of Canada bond yield fell to just under 3.0%, a harbinger of further declines in fixed mortgage rates. The Bank is widely expected to cut the overnight policy rate again by 25 basis points when it meets again on September 4. With good news on the US inflation front, the Fed will likely cut the Fed funds rate as well, its first rate cut this cycle.

Monthly changes in sales activity were generally small amongst the larger centres in July. Interestingly, declines in Calgary and the Greater Toronto Area were offset mainly by gains in Edmonton and Hamilton-Burlington.

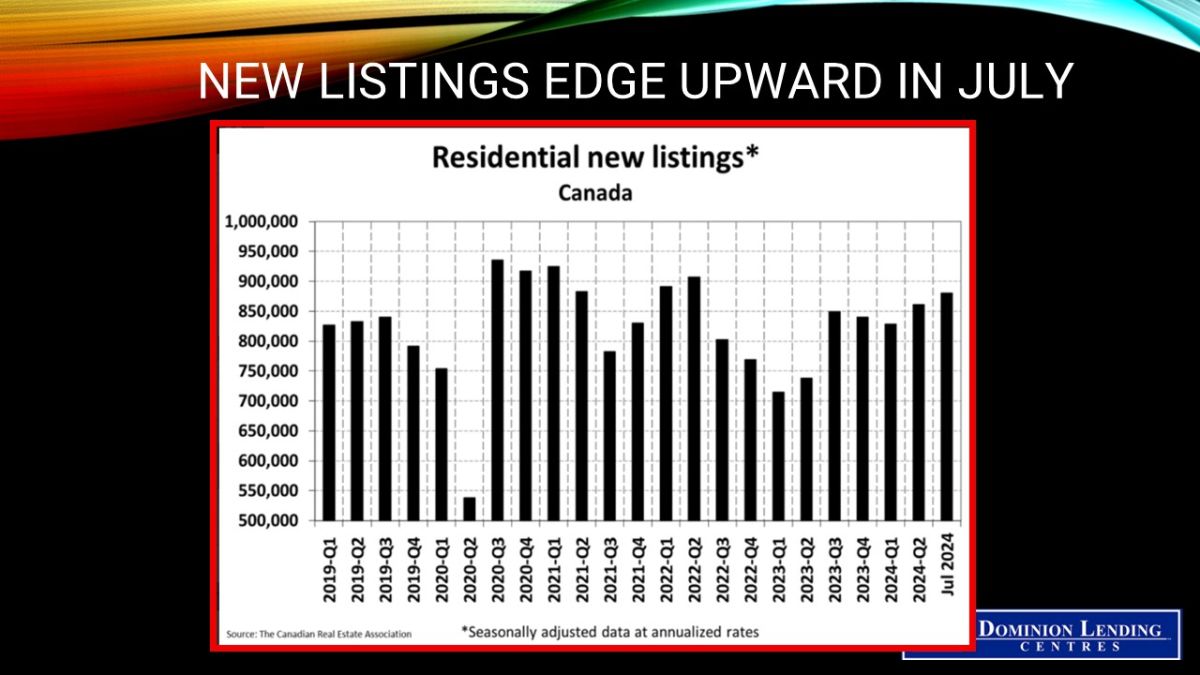

New Listings

As of the end of July 2024, about 183,450 properties were listed for sale on all Canadian MLS® Systems, up 22.7% from a year earlier but still about 10% below historical averages of more than 200,000 for this time of the year.

New listings posted a slight 0.9% month-over-month increase in July. The national increase was led by a much-needed boost in new supply in Calgary.

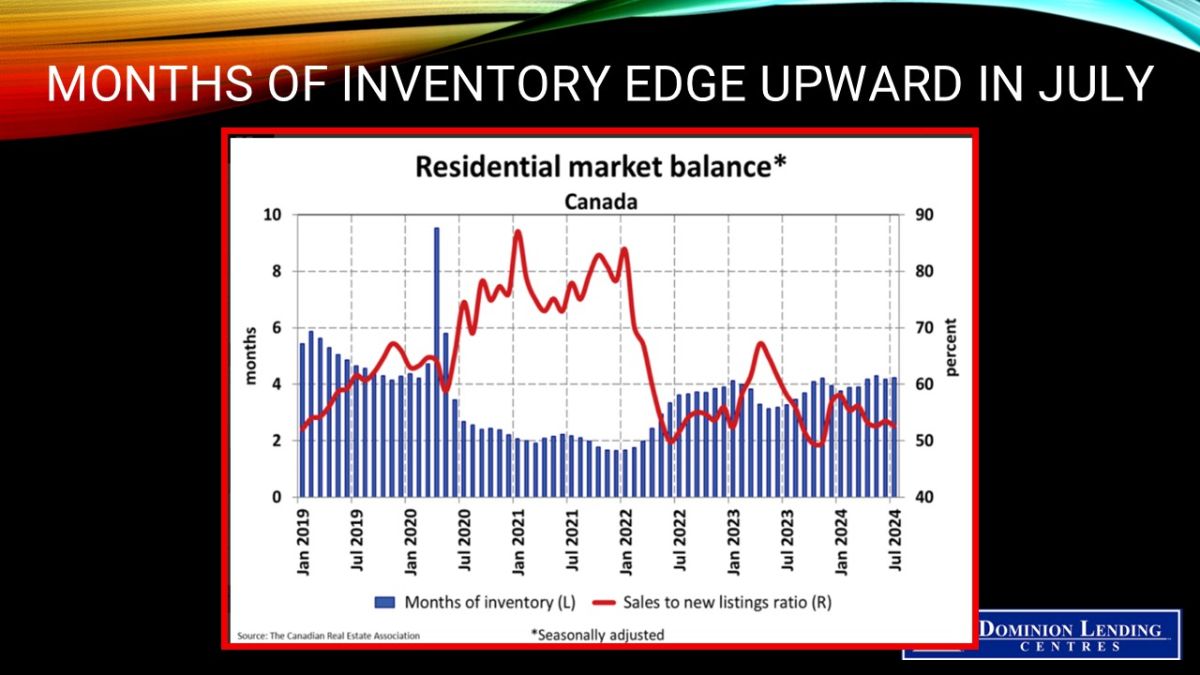

With new listings up slightly and sales down slightly in July, the national sales-to-new listings ratio fell to 52.7% compared to 53.5% in June. The long-term average for the national sales-to-new listings ratio is 55%, with a ratio between 45% and 65% generally consistent with balanced housing market conditions.

There were 4.2 months of inventory nationwide at the end of July, unchanged from the end of June. The long-term average is about five months of inventory.

“While it wasn’t apparent in the July housing data from across Canada, the stage is increasingly being set for the return of a more active housing market,” said James Mabey, Chair of CREA. “At this point, many markets have a healthier amount of choice for buyers than has been the case in recent years, but the days of the slower and more relaxed house hunting experience may be somewhat numbered.

Home Prices

The National Composite MLS® Home Price Index (HPI) increased 0.2% from June to July. While a slight increase, it was slightly larger than the June increase, making it just the second and the most significant gain in the last year.

While prices were up slightly at the national level, they were held back by reduced activity in the largest and most expensive British Columbia and Ontario markets. Regionally, prices are rising in most markets.

The non-seasonally adjusted National Composite MLS® HPI stood 3.9% below July 2023. This primarily reflects how prices took off last April, May, June, and July – something that was not repeated over that same period in 2024. It’s mostly likely that year-over-year comparisons will improve from this point on.

The actual (not seasonally adjusted) national average home price was $667,317 in July 2024, almost unchanged (-0.2%) from July 2023.

Bottom Line

Housing activity will gradually accelerate over the next year as interest rates continue to fall. Many buyers remain on the sidelines awaiting additional interest rate cuts, likely for the remainder of this year and well into 2025. The Bank of Canada will reduce the overnight rate from today’s 4.5% level to roughly 2.75% next year. While housing affordability remains a problem, pent-up demand is mounting, and construction activity is strong. Renewed interest in home purchases is likely during the back-to-school season.