Articles

Posted on September 17, 2024

Great News On the Canadian Inflation Front in August

More Good News On The Canadian Inflation Front

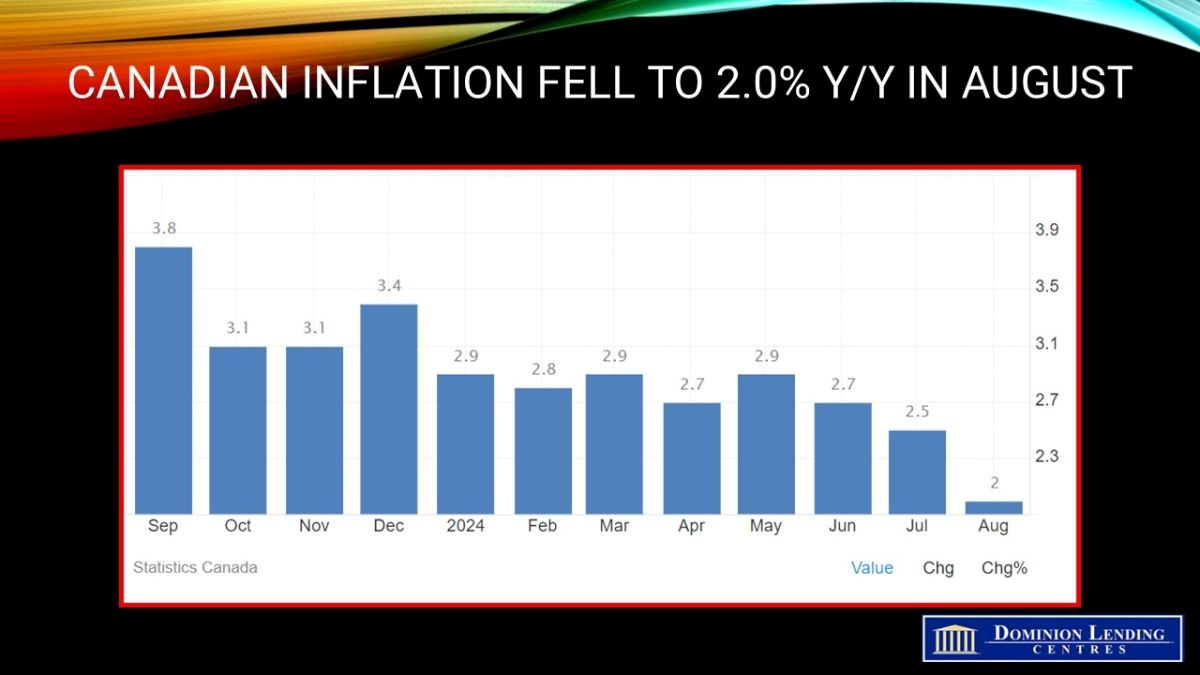

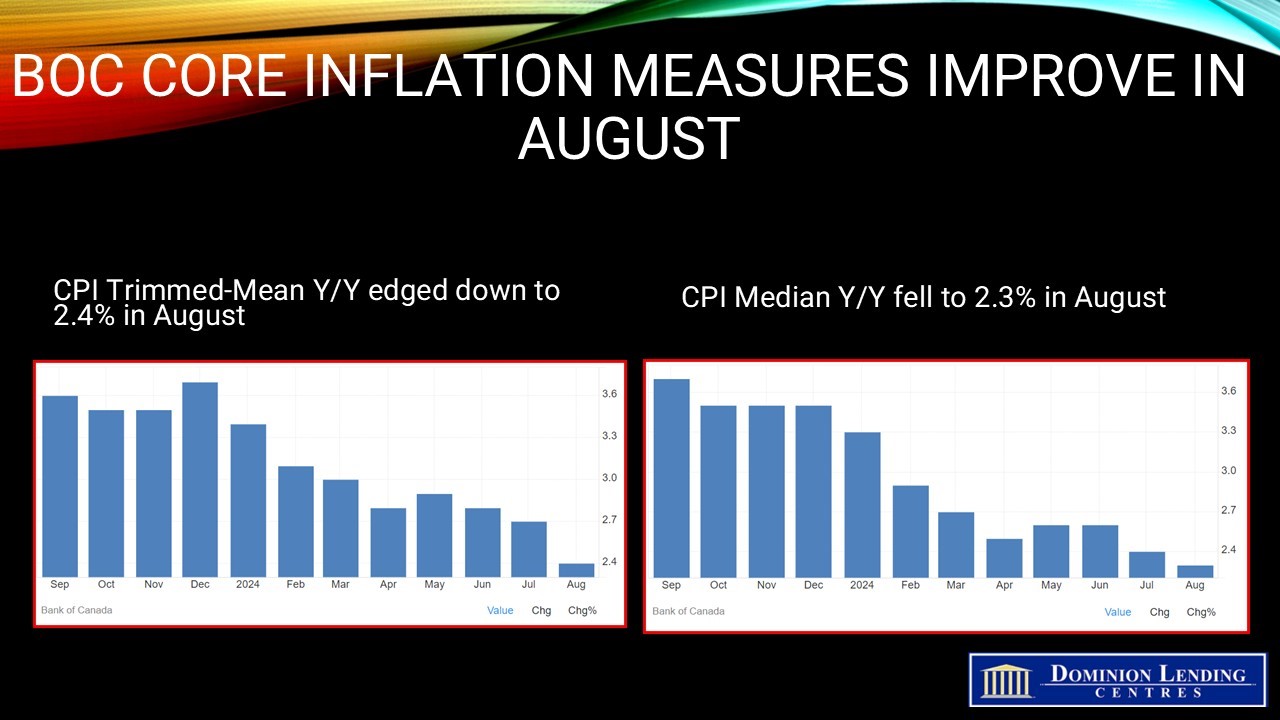

The Consumer Price Index (CPI) rose 2.0% year over year in August, the slowest pace since February 2021, and down from a 2.5% gain in July 2024. Core inflation measures averaged 2.35% y/y and excluding mortgage interest, headline inflation was a mere 1.2%–well below the Bank’s target inflation level of 2.0%. This opens the door for a possible acceleration in Bank of Canada easing. Governor Macklem has suggested that a 50 bp rate cut is possible if inflation falls too fast as unemployment rises.

The deceleration in headline inflation in August was due, in part, to lower gasoline prices, a combination of lower prices and a base-year effect. The decline in August 2024 was mainly due to lower crude oil prices amid economic concerns in the United States and slowing demand in China. Excluding gasoline, the CPI rose 2.2% in August, down from 2.5% in July.

Mortgage interest costs and rent remained the most significant contributors to the increase in the CPI in August. The mortgage interest cost index continued to rise at a slower pace year over year in August (+18.8%) for the 12th consecutive month after peaking in August 2023 (+30.9%). The CPI fell 0.2% m/m in August after increasing 0.4% in July. Lower prices for air transportation, gasoline, clothing and footwear, and travel tours led to a monthly decline. The CPI rose 0.1% in August on a seasonally adjusted monthly basis.

The central bank’s two core inflation measures decreased, averaging a 2.35% yearly pace from 2.55% a month earlier, matching expectations. According to Bloomberg calculations, a three-month moving average of those measures fell to an annualized pace of 2.4% from 2.8% in July.

August marked the eighth month of headline rates within the central bank’s target range.

Bottom Line

The inflation print is the first of two CPI reports before the Bank of Canada’s next rate decision on Oct. 23. After the data were released, overnight swaps traders upped their bets on a larger-than-normal reduction at that decision, putting the odds of a 50-basis point cut at just over a coin flip. Prices declined in five of eight subsectors every month, which could trigger worries about deflation among central bank officials if it becomes a trend. Macklem has recently said the bank cares as much about undershooting the 2% inflation target as it overshooting it.

Markets now suggest a 47% chance of a 50 bps BoC cut on October 23 and a 57% probability of a 25 bps cut. Next week’s GDP data and the October 15 CPI report loom large in the 25 versus 50 bps debate.

Further rate cuts will no doubt spur a housing recovery, though we suspect a shallow one initially due to affordability issues in Ontario and B.C. However, three new mortgage rule changes (effective December 15) could speed things along. The changes will allow all buyers to get a longer 30-year mortgage for a new build, first-time buyers to get a similar term for all properties (both new and old), and buyers to get an insured loan on a home priced up to $1.5 million (versus $1.0 million currently). The latter change will allow smaller down payments and lower borrowing costs than an uninsured loan. The 5-year extended term will lower monthly mortgage payments by about 9%.

June 22, 2026

Canadian Inflation Rises to Highest Level Since 2023 on the Back of a Spike in Gasoline Prices

June 16, 2026

National home sales jumped 5.5% m/m in May as new listings edged down and the Home Price Index (HPI) was down a meagre 0.1% m/m.

June 10, 2026